**Section II. INVESTORS AND MARKETS

****PART ONE. INVESTMENT DECISION RULES

Chapter 15. THE FINANCIAL MARKETS

Now let’s talk finance

This section will analyse the behaviour of the investor who buys financial instruments that the financial manager is trying to sell. Investors are free to buy a security or not and, if they decide to buy it, they are then free to hold it or resell it in the secondary market.

The financial investor seeks two types of returns: the risk-free interest rate (which we call the time value of money) and a reward for risk-taking. This section looks at these two types of returns in detail but, first, here are some general observations about financial markets.

Section 15.1 THE ROLE OF CAPITAL MARKETS

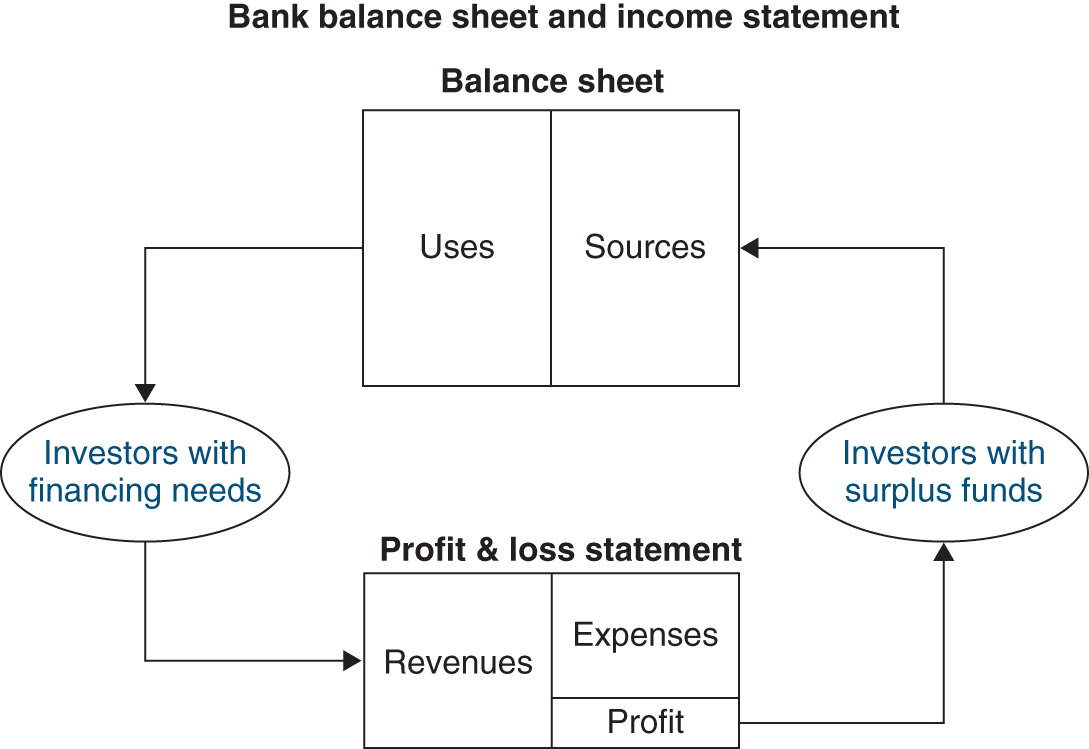

The primary role of a financial system is to bring together economic agents with surplus financial resources, such as households, and those with net financial needs, such as companies and governments. This relationship is illustrated below:

To use the terminology of John Gurley and Edward Shaw (1960), the parties can be brought together directly or indirectly.

In the first case, known as direct finance, the parties with excess financial resources directly finance those with financial needs. The financial system serves as a broker, matching the supply of funds with the corresponding demand. This is what happens when an individual shareholder subscribes to a listed company’s share issue or when a bank places a corporate bond issue with individual investors.

In the second case, or indirect finance, financial intermediaries, such as banks, buy “securities” – i.e. loans – “issued” by companies. The banks in turn collect funds, in the form of demand or savings deposits, or issue their own securities that they place with investors. In this model, the financial system serves as a gatekeeper between suppliers and users of capital and performs the function of intermediation.

When you deposit money in a bank, the bank uses your money to make loans to companies. Similarly, when you buy bonds issued by a financial institution, you enable the institution to finance the needs of other industrial and commercial enterprises through loans. Lastly, when you buy an insurance policy, you and other investors pay premiums that the insurance company uses to invest in the bond market, the property market, etc.

This activity is called intermediation, and is very different from the role of a mere broker in the direct finance model.

With direct finance, the amounts that pass through the broker’s hands do not appear on its balance sheet, because all the broker does is to put the investor and issuer in direct contact with each other. Only brokerage fees and commissions appear on a brokerage firm’s profit and loss, or income, statement.

In intermediation, the situation is very different. The intermediary shows all resources on the liabilities side of its balance sheet, regardless of their nature: from deposits to bonds to shareholders’ equity. Capital serves as the creditors’ ultimate guarantee. On the assets side, the intermediary shows all uses of funds, regardless of their nature: loans, investments, etc. The intermediary earns a return on the funds it employs and pays interest on the resources. These cash flows appear in its income statement in the form of revenues and expenses. The difference, or spread, between the two constitutes the intermediary’s earnings.

The intermediary’s balance sheet and income statement thus function as holding tanks for both parties – those who have surplus capital and those who need it:

Today’s economy is experiencing increasing disintermediation, characterised by the following phenomena:

- more companies are obtaining financing directly from capital markets; and

- more companies and individuals are investing directly in capital markets.

When capital markets are underdeveloped, an economy functions primarily on debt financing. Conversely, when capital markets are sufficiently well developed, companies are no longer restricted to debt, and they can then choose to increase their equity financing. Taking a page from the economist John Hicks, it is possible to speak of bank-based economies and market-based economies.

In a bank-based economy, the capital market is underdeveloped and only a small portion of corporate financing needs are met through the issuance of securities. Therefore, bank financing predominates. Companies borrow heavily from banks, whose refinancing needs are mainly covered by the central bank.

The lender’s risk is that the corporate borrower will not generate enough cash flow to service the debt and repay the principal, or amount of the loan.

In a market-based economy, companies cover most of their financing needs by issuing financial securities (shares, bonds, commercial paper, etc.) directly to investors. A capital market economy is characterised by direct solicitation of investors’ funds. Economic agents with surplus resources invest a large portion of their funds directly in the capital markets by buying companies’ shares, bonds, commercial paper or other short-term negotiable debt. They do this either directly or through mutual funds. Intermediation gives way to the brokerage function, and the business model of financial institutions evolves towards the placement of companies’ securities directly with investors.

In this economic model, bank loans are extended primarily to households in the form of consumer credit, mortgage loans, etc., as well as to small enterprises that do not have access to the capital markets.

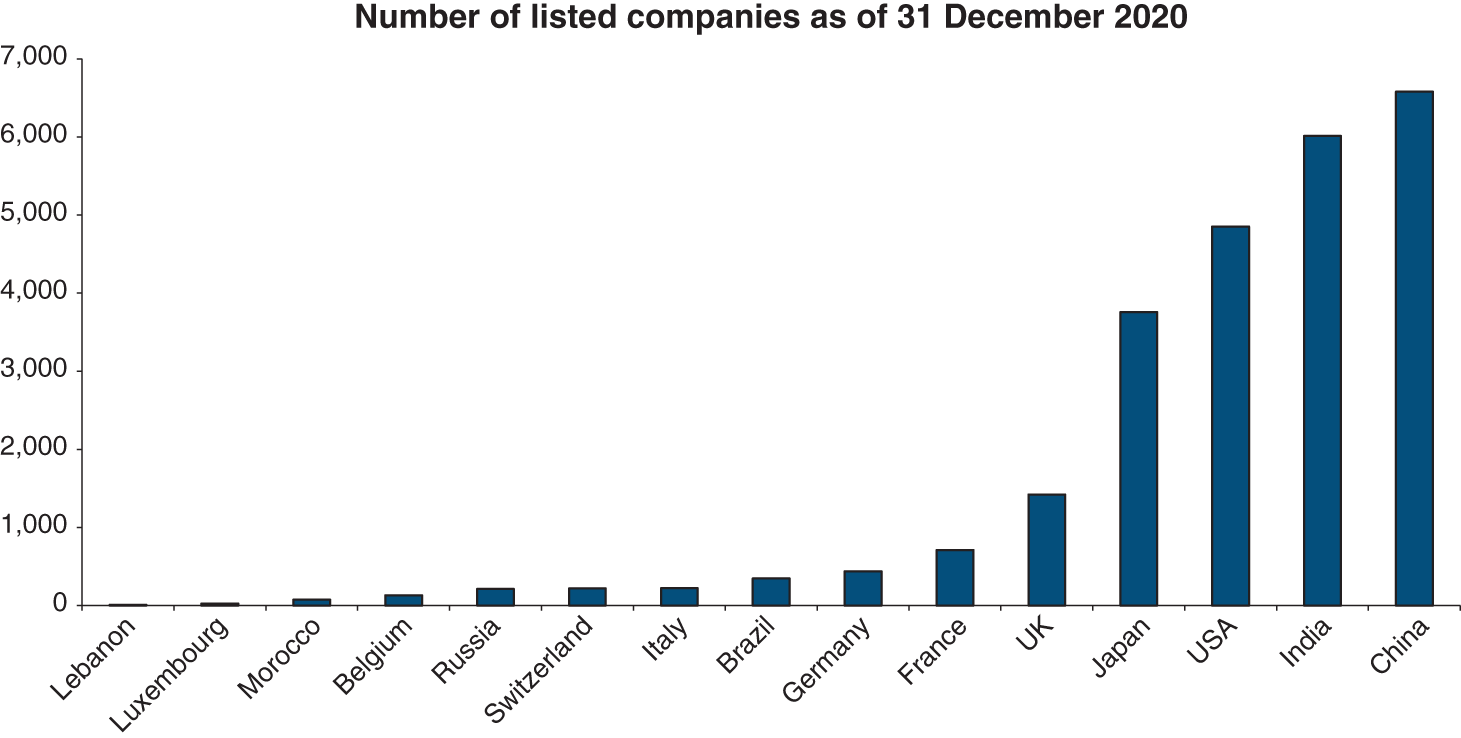

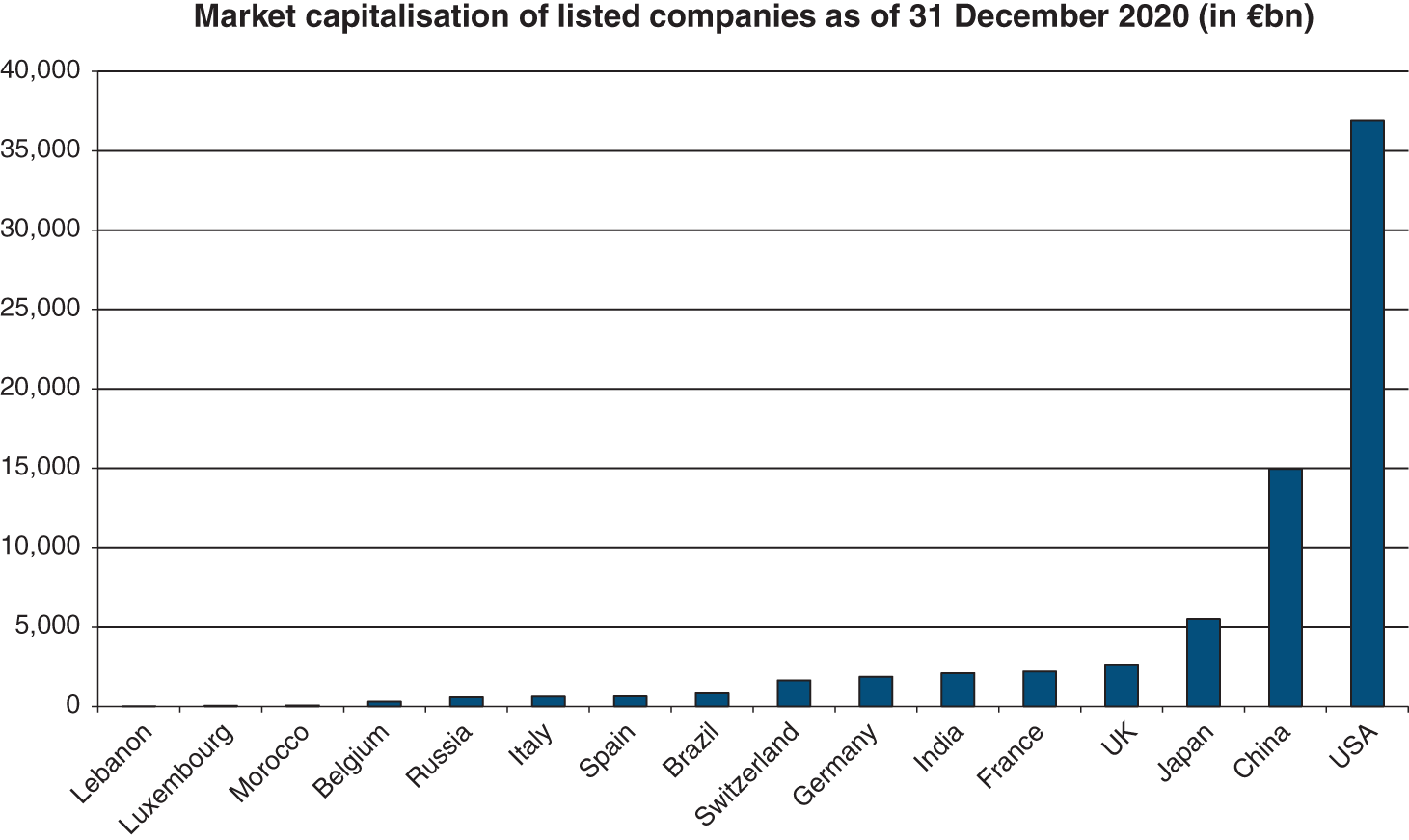

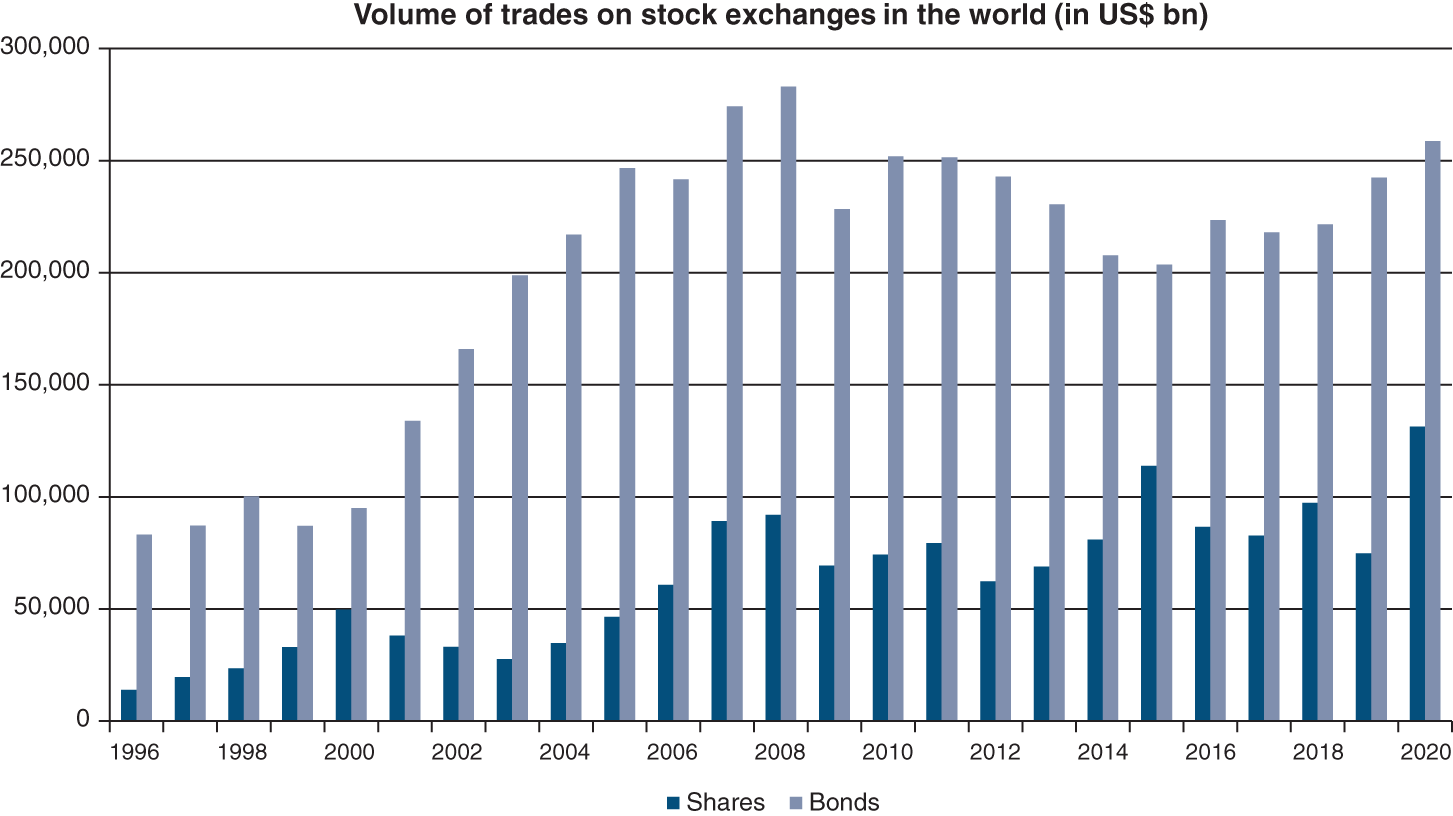

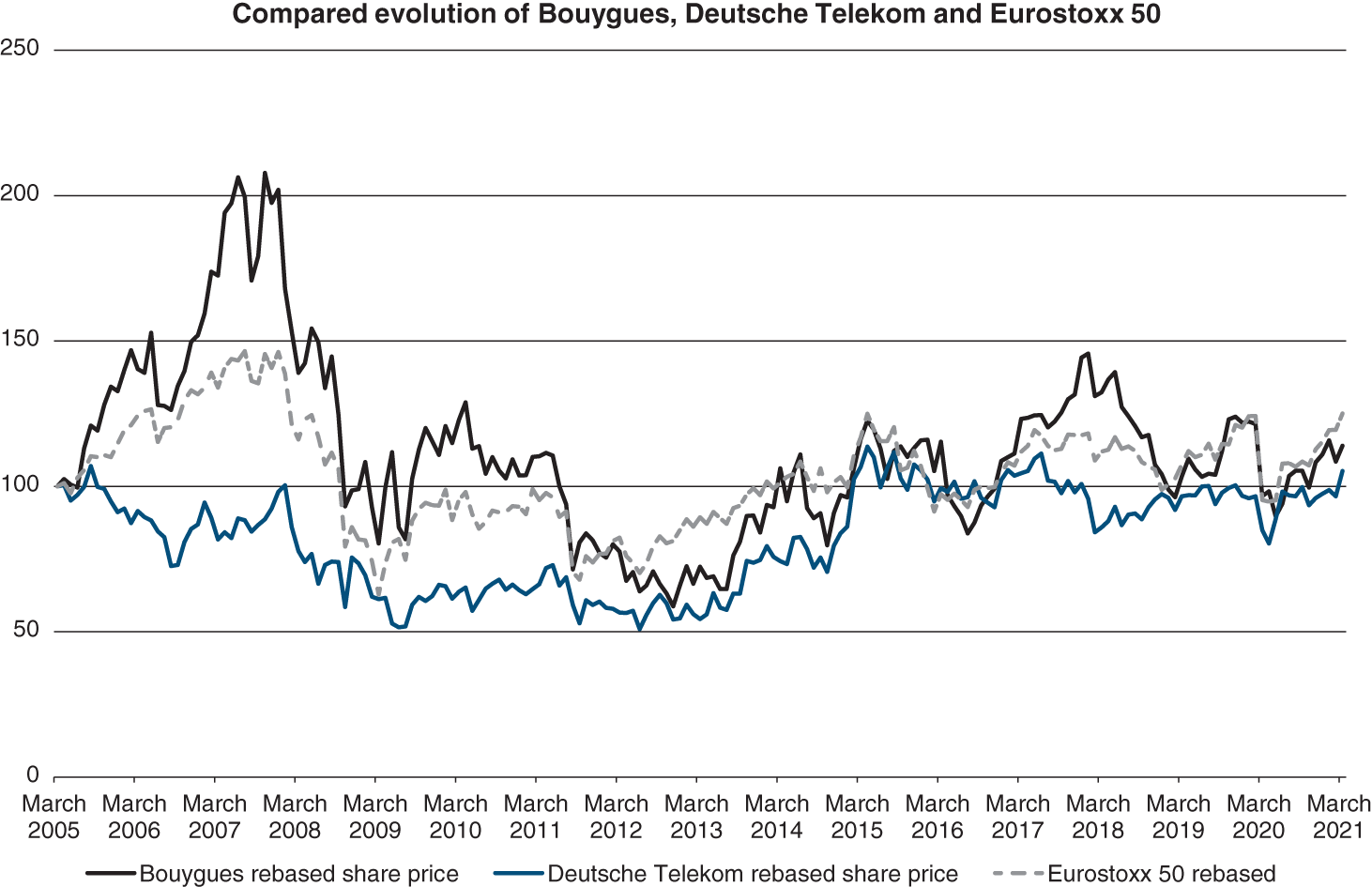

The following graphs provide the best illustration of the rising importance of capital markets.

…be it in terms of the number of listed companies…

Note: Domestic companies only.

Source: Data from World Federation of Exchanges, NYSE-Euronext, London Stock Exchange, Bourse de Casablanca, Bolsa Madrid, Beirut Stock Exchange, Borsa Italiana

Source: Data from World Federation of Exchanges, NYSE-Euronext, Beirut Stock exchange, Borsa Italiana, London Stock Exchange

Source: Data from World Federation of Exchanges, SIFMA

Section 15.2 PRIMARY, SECONDARY AND DERIVATIVE MARKETS

1/ FROM THE PRIMARY MARKET TO THE SECONDARY MARKET

The new issues market (i.e. creation of securities) is called the primary market. Subsequent transactions involving these securities take place on the secondary market. Both markets, like any market, are defined by two basic elements: the product (the security) and the price (its value).

Thus, shares issued or created when a company is founded can later be floated on a stock exchange, just as long-term bonds may be used by speculators for short-term strategies. The life of a financial security is intimately connected with the fact that it can be bought or sold at any moment.

From the point of view of the company, the distinction between the primary and secondary markets is fundamental. The primary market is the market for “new” financial products, from equity issues to bond issues and everything in between. It is the market for newly minted financial securities where the company can raise fresh money.

Conversely, the secondary market is the market for “used” financial products. Securities bought and sold on this market have already been created and are now simply changing hands, without any new securities being created and consequently without any new money for the company.

The primary market enables companies, financial institutions, governments and local authorities to obtain financial resources by issuing securities. These securities are then listed and traded on secondary markets. The job of the secondary market is to ensure that securities are properly priced and traded. This is the essence of liquidity: facilitating the purchase or sale of a security.

The distinction between primary and secondary markets is conceptual only. The two markets are not separated from each other. A given financial investor can buy either existing shares or new shares issued during a capital increase, for example.

If there is often more emphasis placed on the primary market, it is because the function of the financial markets is, first and foremost, to ensure equilibrium between financing needs and the sources of finance. Secondary markets, where securities can change hands, constitute a kind of financial “innovation”.

2/ THE FUNCTION OF THE SECONDARY MARKET

Financial investors do not intend to remain invested in a particular asset indefinitely. Even before they buy a security, they begin thinking about how they will exit. As a result, they are constantly evaluating whether they should buy or sell such and such an asset.

Monetising is relatively easy when the security is a short-term one. All the investor has to do is wait until maturity. The need for an exit strategy grows with the maturity of the investment and is greatest for equity investments, whose maturity is unlimited. The only way a shareholder can exit their investment is to sell their shares to someone else.

As an example, the successful business person who floats their company on the stock exchange, thereby selling part of their shares to new shareholders, diversifies their own portfolio, which before flotation was essentially concentrated in one investment.

Liquidity refers to the ability to convert an instrument into cash quickly and without loss of value. It affords the opportunity to trade a financial instrument at a “listed” price and in large quantities without disrupting the market. An investment is liquid when an investor can buy or sell it in large quantities without causing a change in its market price.

The secondary market is therefore a zero-sum game between investors, because what one investor buys, another investor sells. In principle, the secondary market operates completely independently from the issuer of the securities.

A company that issues a bond today knows that a certain amount of funds will remain available in each future year. This knowledge is based on the bond’s amortisation schedule. During that time, however, the investors holding the bonds will have changed.

Secondary market transactions do not show up in macroeconomic statistics on capital formation, earning them the scorn of some observers who claim that the secondary market does nothing to further economic development, but only bails out the initial investors.

We believe this thinking is misguided and reflects great ignorance about the function of secondary markets in the economy. Remember that a financial investor is constantly comparing the primary and secondary markets. They care little whether a “new” or a “used” security is being bought, so long as they have the same characteristics.

In fact, the quality of a primary market for a security depends greatly on the quality of its secondary market. Think about it: who would want to buy a financial security on the primary market, knowing that it will be difficult to sell it on the secondary market?

The secondary market determines the price at which the company can issue its securities on the primary market, because investors are constantly deciding between existing investments and proposed new investments.

We have seen that it would be a mistake to think that a financial manager takes no interest in the secondary market for the securities issued by the company. On the contrary, it is on the secondary market that the company’s financial “raw material” is priced every day. When the raw material is equities, there is another reason the company cannot afford to turn its back on the secondary market: this is where investors trade the voting rights in the company’s affairs and, by extension, control of the company.

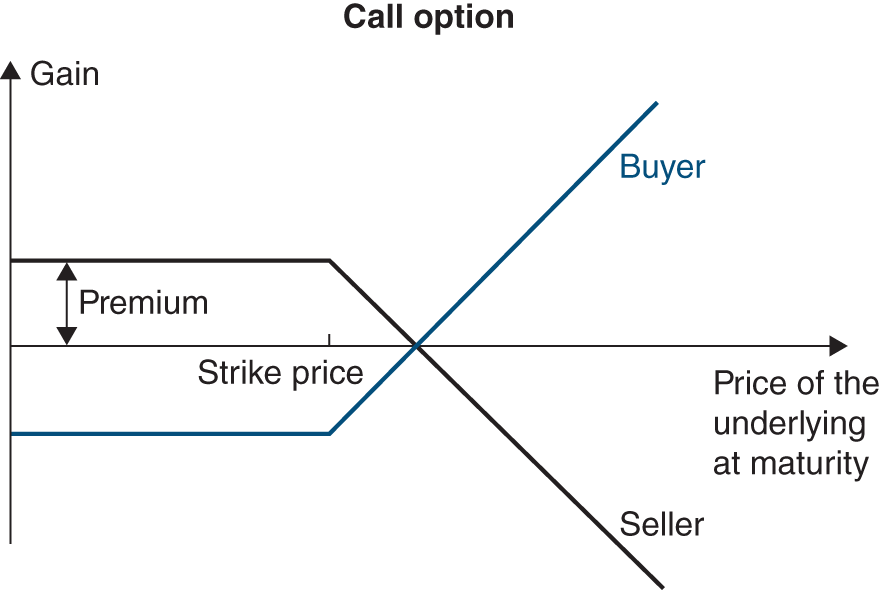

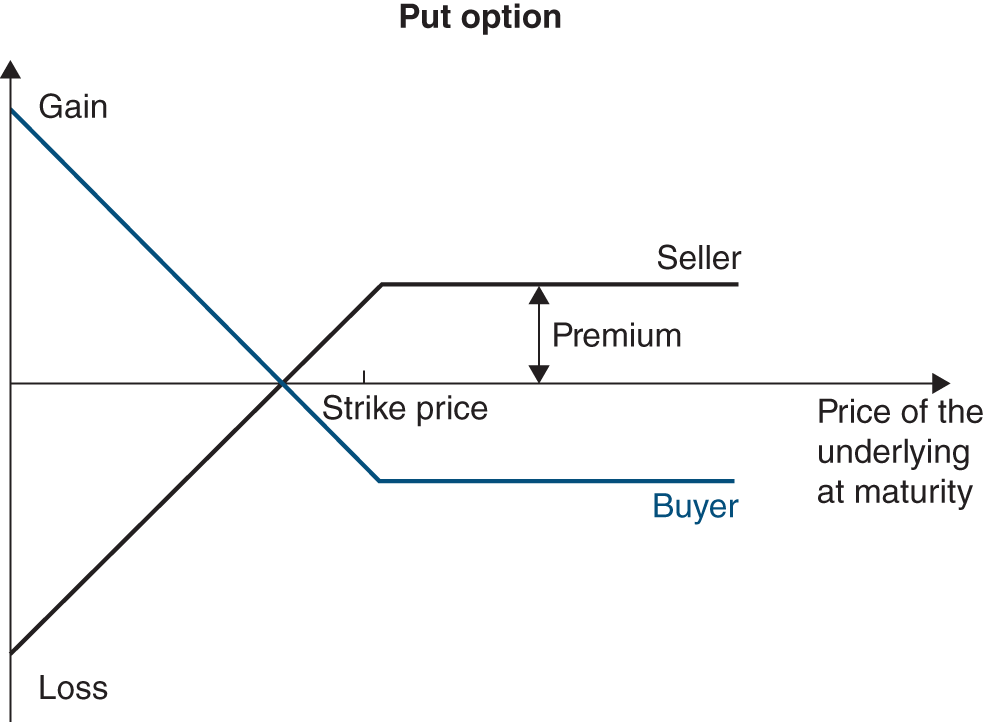

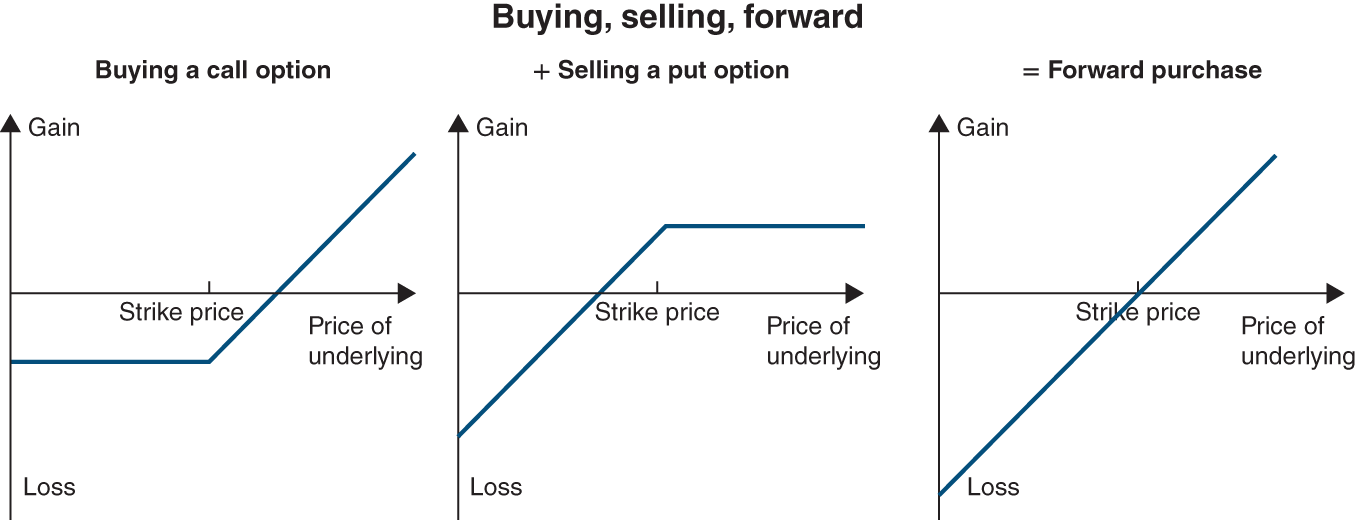

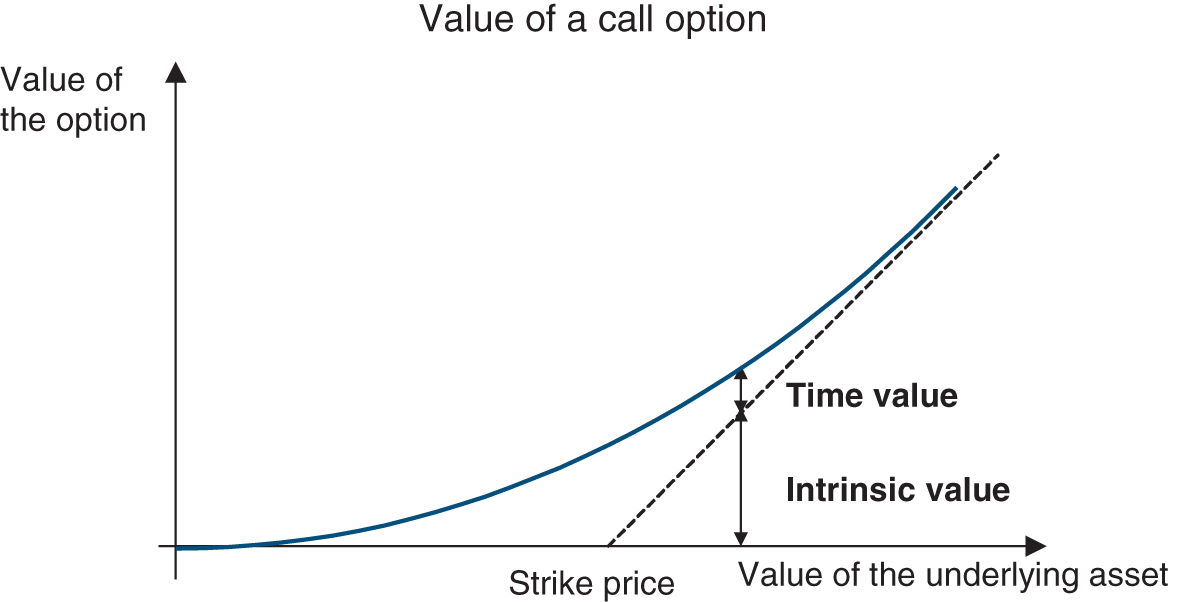

3/ DERIVATIVE MARKETS: FUTURES AND OPTIONS

Derivative markets are where securities that derive their value from another asset (share, bond, commodity or even climate index) are traded. There are two main types of derivative products: options (which we will develop in Chapter 23 as they have become a key matter in financial theory and practice) and futures (Chapter 51).

Derivative instruments are tailored especially to the management of financial risk. By using derivatives, the financial manager chooses a price – expressed as an interest rate, an exchange rate or the price of a raw material – that is independent of the company’s financing or investment term. Derivatives are also highly liquid. The financial manager can change their mind at any time at a minimal cost.

Options and futures allow one to take important risks with a reduced initial outlay due to their leverage effect (this is called speculation), or on the contrary to transfer risks to a third party (hedging), and this is what companies normally use them for.

Section 15.3 THE FUNCTIONS OF A FINANCIAL SYSTEM

The job of a financial system is to efficiently create financial liquidity for those investment projects that promise the highest profitability and that maximise collective utility.

However, unlike other types of markets, a financial system does more than just achieve equilibrium between supply and demand. A financial system allows investors to convert current revenues into future consumption. It also provides current resources for borrowers, at the cost of reduced future spending.

Robert Merton and Zvi Bodie have isolated six essential functions of a financial system:

- A financial system provides means of payment to facilitate transactions. Cheques, debit and credit cards, electronic transfers, bitcoins, etc. are all means of payment that individuals can use to facilitate the acquisition of goods and services. Imagine if everything could only be paid for with bills and coins!

- A financial system provides a means of pooling funds for financing large, indivisible projects. A financial system is also a mechanism for subdividing the capital of a company so that investors can diversify their investments. If factory owners had to rely on just their own savings, they would very soon run out of investible funds. Indeed, without a financial system’s support, Nestlé and British Telecom would not exist. The system enables the entrepreneur to gain access to the savings of millions of individuals, thereby diversifying and expanding their sources of financing. In return, the entrepreneur is expected to achieve a certain level of performance. Returning to our example of a factory, if you were to invest in your neighbour’s steel plant, you might have trouble getting your money back if you should suddenly need it. A financial system enables investors to hold their assets in a much more liquid form: shares, bank accounts, etc.

- A financial system distributes financial resources across time and space, as well as between different sectors of the economy. The financial system allows capital to be allocated in a myriad of ways. For example, young people can borrow to buy a house or people approaching retirement can save to offset future decreases in income. Even a developing nation can obtain resources to finance further development. And when an industrialised country generates more savings than it can absorb, it invests those surpluses through financial systems. In this way, “old economies” use their excess resources to finance “new economies”.

- A financial system provides tools for managing risk. It is particularly risky (and inefficient as we will see later) for an individual to invest all of their funds in a single company because, if the company goes bankrupt, they lose everything. By creating collective savings vehicles, such as mutual funds, brokers and other intermediaries enable individuals to reduce their risk by diversifying their exposure. Similarly, an insurance company pools the risk of millions of people and insures them against risks they would otherwise be unable to assume individually.

- A financial system provides price information at very low cost. This facilitates decentralised decision-making. Asset prices and interest rates constitute information used by individuals in their decisions about how to consume, save or divide their funds among different assets. But research and analysis of the available information on the financial condition of the borrower is time-consuming, costly and typically beyond the scope of the layperson. Yet when a financial institution does this work on behalf of thousands of investors, the cost is greatly reduced.

- A financial system provides the means for reducing conflict between the parties to a contract. Contracting parties often have difficulty monitoring each other’s behaviour. Sometimes conflicts arise because each party has different amounts of information and divergent contractual ties. For example, an investor gives money to a fund manager in the hope that they will manage the funds in the investor’s best interests (and not their own!). If the fund manager does not uphold their end of the bargain, the market will lose confidence in them. Typically, the consequence of such behaviour is that they will be replaced by a more conscientious manager.

Section 15.4 THE RELATIONSHIP BETWEEN BANKS AND COMPANIES

Not so long ago, banks could be classified as:

- Commercial banks that schematically collected funds from individuals and lent to corporates.

- Investment banks that provided advisory services (mergers and acquisitions, wealth management) and played the role of a broker (placement of shares, of bonds) but without “using their balance sheet”.

Since the beginning of this century, large financial conglomerates have emerged both in the US and Europe. This resulted from mega-mergers between commercial banks and investment banks: BNP/Paribas, Citicorp/Travelers Group, Chase Manhattan/JP Morgan, Bank of America/Merrill Lynch, or the transition by investment banks towards commercial banking (Goldman Sachs, Mediobanca) or the reverse (Credit Suisse, Credit Agricole).

This trend, eased by changes in regulation (in particular in the US with the reform of the Glass–Steagall Act in 1999), shows a willingness of large banking groups to adopt the business model of a universal bank (also called “one-stop shopping”) in a context of increasing internationalisation and complexity. This is particularly true for certain business lines like corporate finance or fund management, in which size constitutes a real competitive advantage.

Following the 2008 financial crisis, there emerged a certain political willingness to split up large banking groups again, specifically in order to separate deposits from market-related activities. This idea (not only guided by the protection of households’ deposits) has only partially materialised in laws (in the US, France, the UK) aimed mainly at confining speculative operations and avoiding market activities that put clients’ deposits at risk (Volker regulation in particular).

Large banking groups now generally include the following business lines:

- Retail banking: for individuals and small and medium-sized corporates. Retail banks serve as intermediaries between those who have surplus funds and those who require financing. The banks collect resources from the former and lend money to the latter. They have millions of clients and therefore adopt an industrial organisation. The larger the bank’s portfolio, the lower the risk – thanks once again to the law of large numbers. Retail banking is an extremely competitive activity. After taking into account the cost of risk, profit margins are very thin. Bank loans are somewhat standard products, so it is relatively easy for customers to play one bank off against another to obtain more favourable terms. Retail banks have developed ancillary services to add value to the products that they offer to their corporate customers. Accordingly, they offer a variety of means of payment to help companies move funds efficiently from one place to another. They also help clients to manage their cash flows or their short-term investments (see Chapter 50). A retail banking division also generally includes some specific financial services for individuals (e.g. consumer credit) or for corporates (factoring, leasing, etc.), as such services are used mostly by small and medium-sized firms.

- Corporate and investment banking (CIB): provides large corporates with sophisticated services. Such banks have, at most, a few thousand clients and offer primarily the following services:

- Access to equity markets (equity capital markets, ECM): investment banks help companies prepare and carry out initial public offerings on the stock market. Later on, investment banks can continue to help these companies by raising additional funds through capital increases. They also advise companies on the issuance of instruments that may one day become shares of stock, such as warrants and convertible bonds (see Chapter 24) or the disposal of blocks of a listed subsidiary.

- Access to bond markets (debt capital markets, DCM): similarly, investment banks help large and medium-sized companies raise funds directly from investors through the issuance of bonds. The techniques of placing securities, and in particular the role of the investment bank in this type of transaction, will be discussed in Chapter 25. The investment bank’s trading room is where its role as “matchmaker” between the investor and the issuer takes on its full meaning.

- Merger and acquisition (M&A) advisory services: these investment banking services are not directly linked to corporate financing or the capital markets, although a public issue of bonds or shares often accompanies an acquisition (see Chapter 45). The first three activities are called investment banking.

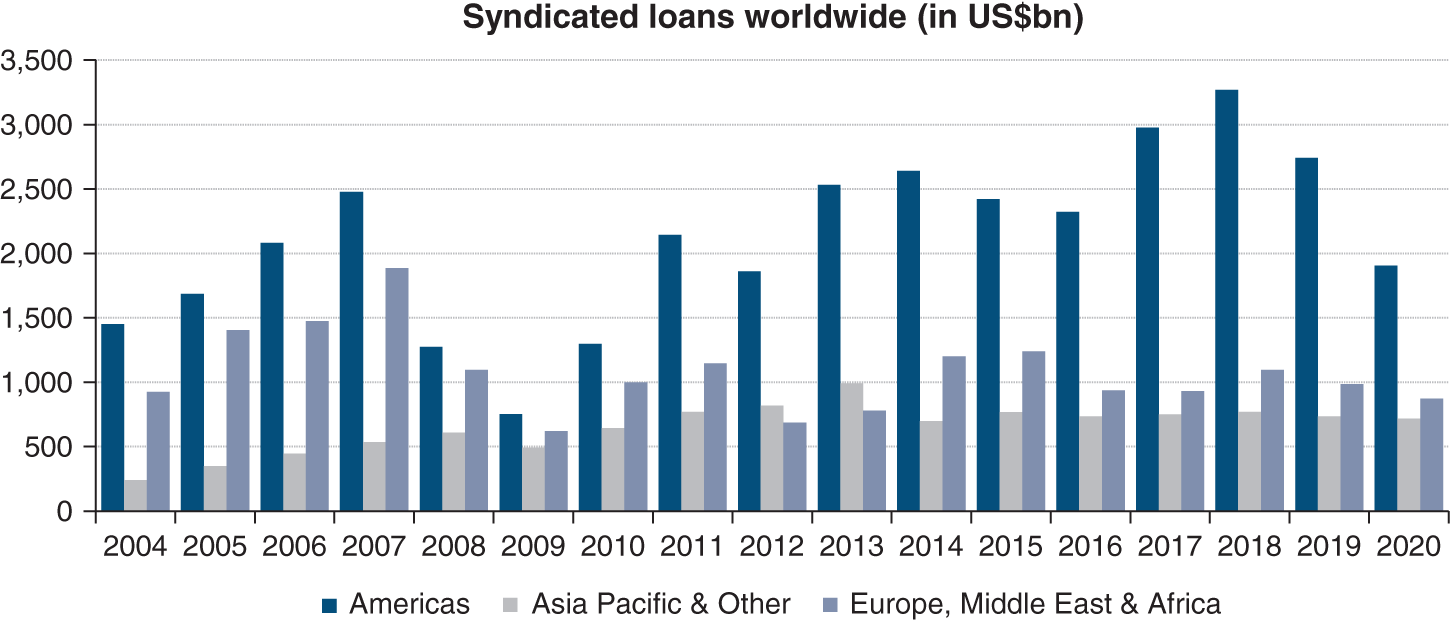

- Bank financing: syndicated loans, bilateral lines, structured financing (see Chapter 21).

- Access to foreign exchange, interest rate and commodities markets: for the hedging of risk. The bank also uses these desks for speculating on its own account (see Chapter 51).

- Asset management: has its own clients – institutional investors and high-net-worth individuals – but also serves some of the retail banking clients through mutual funds. The asset management arm may sometimes use some of the products tailored by the investment banking division (hedging, order execution). This business is increasingly operated by players that are independent (totally or partially) from large banks.

Besides these global banking groups operating across all banking activities, some players have focused on certain targeted services like mergers and acquisitions and asset management (Lazard and Rothschild, for example), retail (it is the case for internet based new banks like N26, Revolut or Orange Bank) or specific geographical areas (Mediobanca and Lloyds Bank, for example).

The 2020 crisis (after 2008) demonstrated again the central role played by banks in the economy. They are suppliers of liquidity; they are also an indicator of investor risk aversion. The basic duty of a bank is to assess risk and repackage it while eliminating the diversifiable risk.

Section 15.5 THEORETICAL FRAMEWORK: EFFICIENT MARKETS

In an efficient market, prices instantly reflect the consequences of past events and all expectations about future events. As all known factors are already integrated into current prices, it is therefore impossible to predict future variations in the price of a financial instrument. Only new information will change the value of the security. Future information is, by definition, unpredictable, so changes in the price of a security are random. This is the origin of the random walk character of daily returns in the securities markets.

Competition between financial investors is so fierce that prices adjust to new information almost instantaneously. At every moment, a financial instrument trades at a price determined by its return and its risk as perceived by its investors.

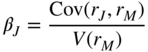

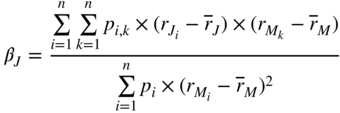

Eugene Fama (1970) has developed the following three tests to determine whether a market is efficient: ability to predict future prices, market response to specific events, impact of insider information on the market.

In a weak-form efficient market, it is impossible to predict future returns. Existing prices already reflect all the information that can be gleaned from studying past prices and trading volumes. The efficient market hypothesis says that technical analysis has no practical value, nor do martingales (martingales in the ordinary, not the mathematical, sense). For example, the notion that “if a stock rises three consecutive times, buy it; if it declines two consecutive times, sell it” is irrelevant. Similarly, the efficient market hypothesis says that models relating future returns to interest rates, dividend yields, the spread between short- and long-term interest rates or other parameters are equally worthless.

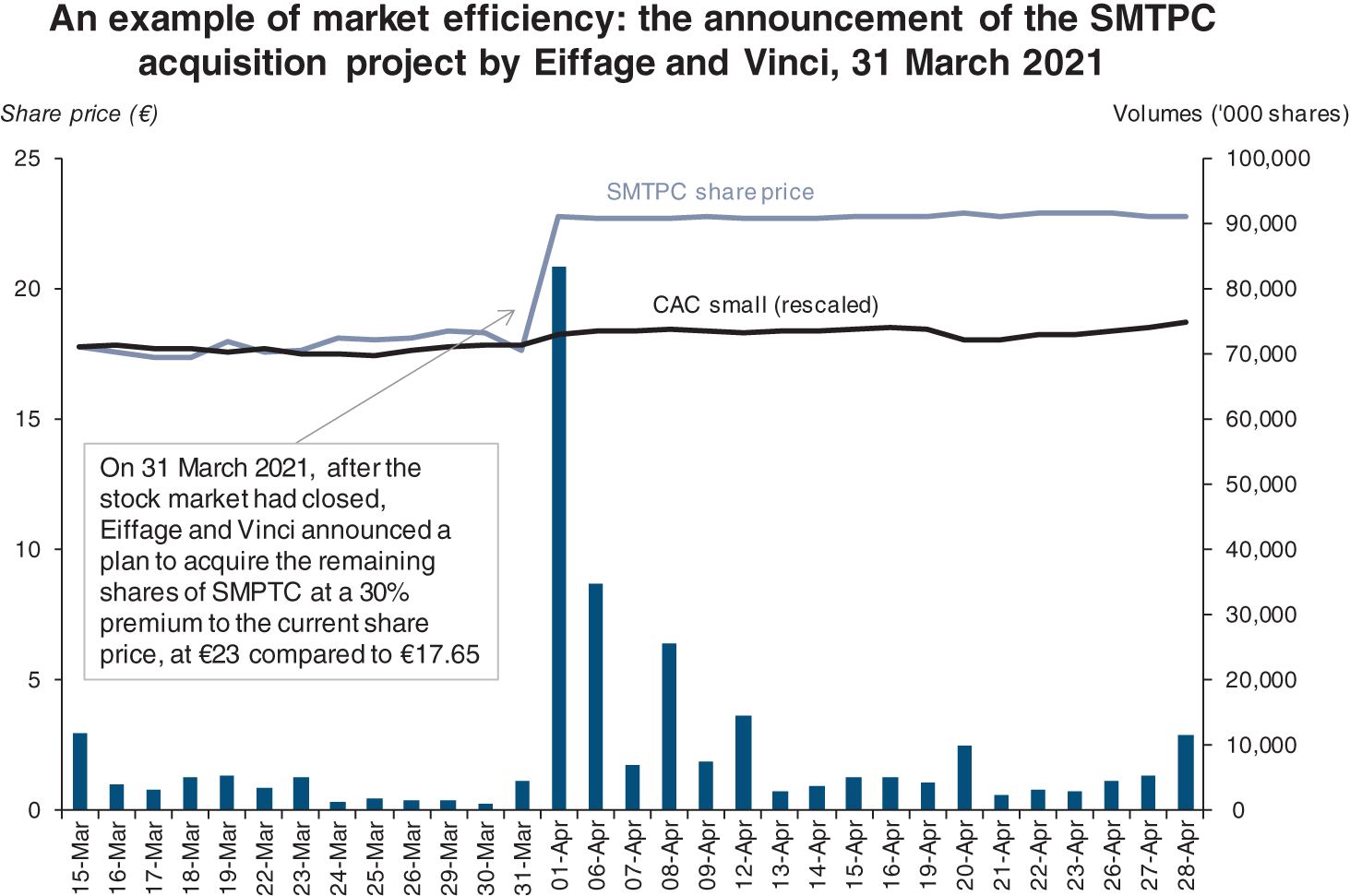

A semi-strong efficient market reflects all publicly available information, as found in annual reports, newspaper and magazine articles, prospectuses, announcements of new contracts, of a merger, of an increase in the dividend, etc. This hypothesis can be empirically tested by studying the reaction of market prices to company events (event studies). In fact, the price of a stock reacts immediately to any announcement of relevant new information regarding a company. In an efficient market, no impact should be observable prior to the announcement, nor during the days following the announcement. In other words, prices should adjust rapidly only at the time any new information is announced.

Source: Data from Euronext

In order to prevent investors with prior access to information from using it to their advantage (and therefore to the detriment of other investors), stock market regulators suggest that firms communicate before market opening or after market closure, or suspend trading prior to a mid-session announcement of information that is highly likely to have a significant impact on the share price. Trading resumes a few hours later or the following day so as to ensure that all interested parties receive the information. Then, when trading resumes, no investor has been short-changed.

In a strongly efficient financial market, investors with privileged or insider information or with a monopoly on certain information are unable to influence securities prices. This holds true only when financial market regulators have the power to prohibit and punish the use of insider information.

In theory, professional investment managers have expert knowledge that is supposed to enable them to post better performances than the market average. However, without using any inside information, the efficient market hypothesis says that market experts have no edge over the layperson. In fact, in an efficient market, the experts’ performance is slightly below the market average, in a proportion directly related to the management fees they charge!

Actual markets approach the theory of an efficient market when participants have low-cost access to all information, transaction costs are low, the market is liquid and investors are rational.

Take the example of a stock whose price is expected to rise 10% tomorrow. In an efficient market, its price will rise today to a level consistent with the expected gain. “Tomorrow’s” price will be discounted to today. Today’s price becomes an estimate of the value of tomorrow’s price.

Section 15.6 ANOTHER THEORETICAL FRAMEWORK UNDER CONSTRUCTION: BEHAVIOURAL FINANCE

Since the end of the 1960s, a large number of research papers have focused on testing the efficiency of markets. It is probably the most tested assumption of finance! Since the early 1980s, researchers (notably Thaler and Kahneman) have highlighted a number of “anomalies” that tend to go against the efficiency of markets:

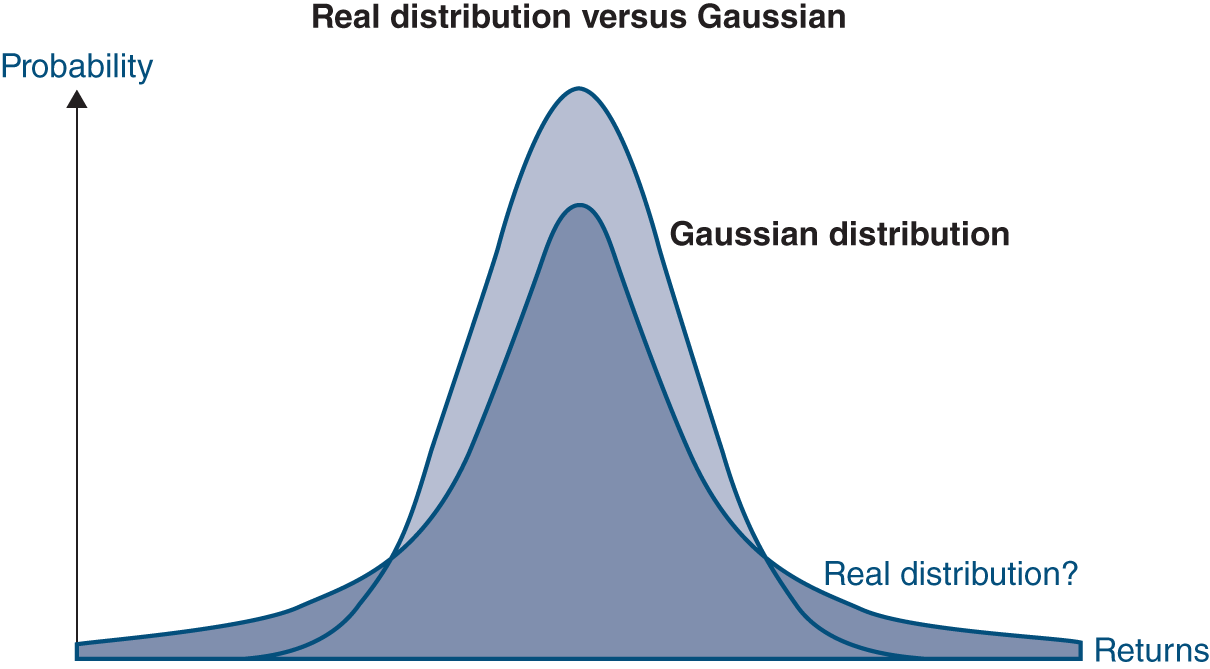

- Excess volatility. The first issue with efficient market theory seems very intuitive: how can markets be so volatile? Information on Sanofi is not published every second. Nevertheless, the share price does move at each instant. There seems to be some kind of noise around fundamental value. As described by Benoit Mandelbrot, who first used fractals in economics, prices evolve in a discrete way rather than in a continuous manner.

- Dual listing and closed-end funds. Dual listings are shares of twin companies listed on two different markets. Their stream of dividends is, by definition, identical but we can observe that their price can differ over a long period of time. Similarly, the price of a closed-end fund (made up of shares of listed companies) can differ from the sum of the value of its components. Conglomerate discount (see Chapter 42) cannot explain the magnitude of the discount for certain funds and certainly not the premium for some others. It is interesting to see that these discounts can prevail over a long period of time, therefore making any arbitrage (although easy to conceptualise) hard to put in place.

- Calendar anomalies. Stocks seem to perform less well on Mondays than on other days of the week and provide higher returns in the month of January compared to other months of the year (in particular for small and medium-sized enterprises). Nevertheless, these calendar anomalies are not material enough to allow for systematic and profitable arbitrage given transaction costs. For each of these observations, some justifications consistent with the rationality of investor behaviour can be put forward.

- Meteorological anomalies. There is consistent observation that stock prices perform better when the sun shines than when it rains. There again, although statistically significant, these anomalies are not material enough to generate arbitrage opportunities.

There are some grounds to think a certain number of situations challenge the validity of the efficient market theory. Nevertheless, Eugene Fama, one of the founders of this theory, defends it strongly. He calls into question the methodologies used to find anomalies. Behavioural finance rejects the founding assumption of market efficiency: what if investors were not rational? It tries to build on other fields of social science to derive new conclusions. For example, economists will work with neuroscientists and psychologists to understand individual economic choices. This allows us to suppose that some decisions are influenced by circumstances and the environment.

One of the first tests for understanding people’s reasoning in making a choice is based on lotteries (gains with certain probabilities). The following attitudes can be observed:

- Gains and losses are not treated equally by investors: they will take risks when the probability of losing is high (they prefer a 50% chance of losing 100 to losing 50 for sure) whereas they will prefer a small gain if the probability is high (getting 50 for sure rather than a 50% chance of 100).

- If the difference (delta) in probability is narrow, the investor will choose the lottery with the highest return possible, but if the delta in probability is high, the investor will think in terms of weighted average return. This may generate some paradoxes: preferring Natixis to UBS, UBS to Mediobanca but Mediobanca to Natixis! This could drive an asset manager mad!

The lack of rationality of some investors would not be a problem if arbitrage made it possible to correct anomalies and if efficiency could be brought back rapidly. Unfortunately, anomalies can be observed over the long term.

The theory of mimicry is an illustration of behavioural finance. The economist André Orléan has distinguished three types of mimicry:

- Normative mimicry – which could also be called “conformism”. Its impact on finance is limited and is beyond the scope of this text.

- Informational mimicry – which consists of imitating others because they supposedly know more. It constitutes a rational response to a problem of dissemination of information, provided the proportion of imitators in the group is not too high. Otherwise, even if it is not in line with objective economic data, imitation reinforces the most popular choice, which can then interfere with efficient dissemination of information.

- Self-mimicry – which attempts to predict the behaviour of the majority in order to imitate it. The “right” decision then depends on the collective behaviour of all other market participants and can become a self-fulfilling prophecy, i.e. an equilibrium that exists because everyone thinks it will exist. This behaviour departs from traditional economic analysis, which holds that financial value results from real economic value.

The surge in the price of the video game company Gamestop, which went from $18 to $325 in 20 days in January 2021, or that of AMC (movie theatres), which went from $13 to $60 in the first half of 2021, are illustrations of a frenetic mimicry, totally disconnected from the economic situation, real or even possible, of these companies. These surges are rooted in the compulsive buying of tens of thousands of people who have never read a single page of the Vernimmen, or any other finance textbook, but who encourage and intoxicate each other on social networks.

Mimetic phenomena can be accentuated by program trading, which involves the computer programs used by some traders that rely on pre-programmed buy or sell decisions. These programs can schedule liquidating a position (i.e. selling an investment) if the loss exceeds a certain level. A practical issue with such programs was illustrated on 21 February 2021 by the flash crash of the bitcoin, which lost 34% before recovering its initial price in just one hour.

If some want to destroy efficient market theory, they will have to propose a viable alternative. As of today, the models proposed by “behaviourists” cannot be used, they merely model the behaviour of investors towards investment decisions and products.

Section 15.7 INVESTORS’ BEHAVIOUR

At any given point in time, each investor is either:

- a hedger;

- a speculator; or

- an arbitrageur.

1/ HEDGING

When an investor attempts to protect himself from risks they do not wish to assume, they are said to be hedging. The term “to hedge” describes a general concept that underlies certain investment decisions, for example, the decision to match a long-term investment with long-term financing, to finance a risky industrial investment with equity rather than debt, etc.

This is simple, natural and healthy behaviour for non-financial managers. Hedging protects a manufacturing company’s margin, i.e. the difference between revenue and expenses, from uncertainties in areas relating to technical expertise, human resources, sales and marketing, etc. Hedging allows the economic value of a project or line of business to be managed independently of fluctuations in the capital markets.

Accordingly, a European company that exports products to the US may sell dollars forward against euros, guaranteeing itself a fixed exchange rate for its future dollar-denominated revenues. The company is then said to have hedged its exposure to fluctuations in currency exchange rates.

2/ SPECULATION

In contrast to hedging, which eliminates risk by transferring it to a party willing to assume it, speculation is the assumption of risk. A speculator takes a position when they make a bet on the future value of an asset. If they think its price will rise, they buy it. If it rises, they win the bet; if not, they lose. If they are to receive dollars in a month’s time, they may take no action now because they think the dollar will rise in value between now and then. If they have long-term investments to make, they may finance them with short-term funds because they think that interest rates will decline in the meantime and they will be able to refinance at lower cost later. This behaviour is diametrically opposed to that of the hedger.

- Traders are professional speculators. They spend their time buying currencies, bonds, shares or options that they think will appreciate in value and they sell them when they think they are about to decline. Not surprisingly, their motto is “Buy low, sell high, play golf!”

- But the investor is also a speculator most of the time. When an investor predicts cash flows, they are speculating about the future. This is a very important point, and you must be careful not to interpret “speculation” negatively. Every investor speculates when they invest, but their speculation is not necessarily reckless. It is founded on a conviction, a set of skills and an analysis of the risks involved. The only difference is that some investors speculate more heavily than others by assuming more risk.

People often criticise the financial markets for allowing speculation. Yet speculators play a fundamental role in the market, an economically healthy role, by assuming the risks that other participants do not want to accept. In this way, speculators minimise the risk borne by others.

Accordingly, a European manufacturing company with outstanding dollar-denominated debt that wants to protect itself against exchange rate risk (i.e. a rise in the value of the dollar vs. the euro) can transfer this risk by buying dollars forward from a speculator willing to take that risk. By buying dollars forward today, the company knows the exact dollar/euro exchange rate at which it will repay its loan. It has thus eliminated its exchange rate risk. Conversely, the speculator runs the risk of a fluctuation in the value of the dollar between the time they sell the dollars forward to the company and the time they deliver them, i.e. when the company’s loan comes due.

Likewise, if a market’s long-term financing needs are not satisfied, but there is a surplus of short-term savings, then sooner or later a speculator will (fortunately) come along and assume the risk of borrowing short term in order to lend long term. In so doing, the speculator assumes intermediation risk.

What, then, do people mean by a “speculative market”? A speculative market is a market in which all the participants are speculators. Market forces, divorced from economic reality, become self-sustaining because everyone is under the influence of the same phenomenon. Once a sufficient number of speculators think that a stock will rise, their purchases alone are enough to make the stock price rise. Their example prompts other speculators to follow suit, the price rises further, and so on. But at the first hint of a downward revision in expectations, the mechanism goes into reverse and the share price falls dramatically. When this happens, many speculators will try to liquidate positions in order to pay off loans contracted to buy shares in the first place, thereby further accentuating the downfall.

3/ ARBITRAGE

In contrast to the speculator, the arbitrageur is not in the business of assuming risk or having a view on future price of an asset. Instead, they try to earn a profit by exploiting tiny discrepancies which may appear on different markets that are not in equilibrium.

An arbitrageur will notice that Solvay shares are trading slightly lower in London than in Brussels. They will buy Solvay shares in London and sell them simultaneously (or nearly so) at a higher price in Brussels. By buying in London, the arbitrageur bids the price up in London; by selling in Brussels, they drive the price down there. They, or other arbitrageurs, then repeat the process until the prices in the two markets are perfectly in line, or in equilibrium.

In principle, the arbitrageur assumes no risk, even though each separate transaction involves a certain degree of risk.

Arbitrage is of paramount importance in a market. By destroying opportunities as it uncovers them, arbitrage participates in the development of new markets by creating liquidity. It also eliminates the temporary imperfections that can appear from time to time. As soon as disequilibrium appears, arbitrageurs buy and sell assets and increase market liquidity. It is through their very actions that the disequilibrium is reduced to zero. Once equilibrium is reached, arbitrageurs stop trading and wait for the next opportunity.

Arbitrage transactions are all the faster to intervene (by computer programs nowadays) when the securities markets are liquid. Otherwise, imbalances may persist for some time on very illiquid securities. Market liquidity and progress in technology make arbitrage opportunities more and more complex and rare. Therefore, some arbitrators are forced in practice to take a certain amount of risk and therefore a speculative component normally foreign to arbitration in the pure sense of the term. In particular, the example given of Solvay is interesting to understand the concept of arbitrage but has not been relevant for quite some time.

Throughout this book, you will see that financial miracles are impossible because arbitrage levels the playing field between assets exhibiting the same level of risk.

You should also be aware that the three types of behaviour described here do not correspond to three mutually exclusive categories of investors. A market participant who is primarily a speculator might carry out arbitrage activities or partially hedge their position. A hedger might decide to hedge only part of their position and speculate on the remaining portion, etc.

The reader will not be fooled by the colloquial use of some words. “Hedge funds” do not operate hedging transactions but are most often involved in speculating. Otherwise, what explanation is there for the fact that they can earn or lose millions of dollars in a few days?

Moreover, these three types of behaviour exist simultaneously in every market. A market cannot function only with hedgers, because there will be no one to assume the risks they don’t want to take.1 As we saw above, a market composed wholly of speculators is not viable either. Finally, a market consisting only of arbitrageurs would be even more difficult to imagine.

SUMMARY

QUESTIONS

ANSWERS

BIBLIOGRAPHY

NOTES

Chapter 16. THE TIME VALUE OF MONEY AND NET PRESENT VALUE

A bird in the hand is worth two in the bush

For economic progress to be possible, in normal economic conditions, there must be a time value of money, even in a risk-free environment. This fundamental concept gives rise to the techniques of capitalisation, discounting and net present value, described below.

Section 16.1 CAPITALISATION

Consider an example of a businessman who invests €100,000 in his business at the end of 2011 and then sells it 10 years later for €1,800,000. In the meantime, he receives no income from his business, nor does he invest any additional funds into it. Here is a simple problem: given an initial outlay of €100,000 that becomes €1,800,000 in 10 years, and without any outside funds being invested in the business, what is the return on the businessman’s investment?

His profit after 10 years was €1,700,000 (€1,800,000 – €100,000) on an initial outlay of €100,000. Hence, his return was (1,700,000 / 100,000) or 1,700% over a period of 10 years.

Is this a good result or not?

Actually, the return is not quite as impressive as it first looks. To find the annual return, our first thought might be to divide the total return (1,700%) by the number of years (10) and say that the average return is 170% per year.

While this may look like a reasonable approach, it is in fact far from accurate. The value 170% has nothing to do with an annual return, which compares the funds invested and the funds recovered after one year. In the case above, there is no income for 10 years. Usually, calculating interest assumes a flow of revenue each year, which can then be reinvested, and which in turn begins producing additional interest.

There is only one sensible way to calculate the return on the above investment. First, it is necessary to seek the rate of return on a hypothetical investment that would generate income at the end of each year. After 10 years, the rate of return on the initial investment will have to have transformed €100,000 into €1,800,000. Further, the income generated must not be paid out, but rather it has to be reinvested (in which case the income is said to be capitalised).

Therefore, we are now trying to calculate the annual return on an investment that grows from €100,000 into €1,800,000 after 10 years, with all annual income to be reinvested each year.

An initial attempt to solve this problem can be made using a rate of return equal to 10%. If, at the end of 2011, €100,000 is invested at that rate, it will produce 10% × €100,000, or €10,000 in interest in 2012.

This €10,000 will then be added to the initial capital outlay and begin, in turn, to produce interest. (Hence the term “to capitalise”, which means to add to capital.) The capital thus becomes €110,000 and produces 10% × €110,000 in interest in 2013, i.e. €10,000 on the initial outlay plus €1,000 on the interest from the €10,000 interest earned in 2012 (10% × €10,000). As the interest is reinvested, the capital becomes €110,000 + €11,000, or €121,000, which will produce €12,100 in interest in 2014, and so on.

If we keep doing this until 2020, we obtain a final sum of €259,374, as shown in the table.

| Year | Capital at the beginning of the period (€) (1) | Income (€) (2) = 10% × (1) | Capital at the end of the period (€) = (1) + (2) |

|---|---|---|---|

| 2012 | 100,000 | 10,000 | 110,000 |

| 2013 | 110,000 | 11,000 | 121,000 |

| 2014 | 121,000 | 12,100 | 133,100 |

| 2015 | 133,100 | 13,310 | 146,410 |

| 2016 | 146,410 | 14,641 | 161,051 |

| 2017 | 161,051 | 16,105 | 177,156 |

| 2018 | 177,156 | 17,716 | 194,872 |

| 2019 | 194,872 | 19,487 | 214,359 |

| 2020 | 214,359 | 21,436 | 235,795 |

| 2021 | 235,795 | 23,579 | 259,374 |

Each year, interest is capitalised and itself produces interest. This is called compound interest. This is easy to express in a formula:

which can be generalised into the following:

where V is a sum and r the rate of return.

Hence, V2012 = V2011 × (1 + 10%), but the same principle can also yield:

All these equations can be consolidated into the following:

Or, more generally:

where V0 is the initial value of the investment, r is the rate of return and n is the duration of the investment in years.

This is a simple equation that gets us from the initial capital to the terminal capital. Terminal capital is a function of the rate r and the duration n.

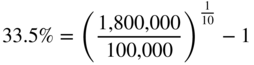

Now it is possible to determine the annual return. In the example, the annual rate of return is not 170%, but 33.5% (which is not bad, all the same!). Therefore, 33.5% is the rate on an investment that transforms €100,000 into €1,800,000 in 10 years, with annual income assumed to be reinvested every year at the same rate.

To calculate the return on an investment that does not distribute income, it is possible to reason by analogy. This is done using an investment that, over the same duration, transforms the same initial capital into the same terminal capital and produces annual income reinvested at the same rate of return. At 33.5%, annual income of €33,500 for 10 years (plus the initial investment of €100,000 paid back after the tenth year) is exactly the same as not receiving any income for 10 years and then receiving €1,800,000 in the tenth year.

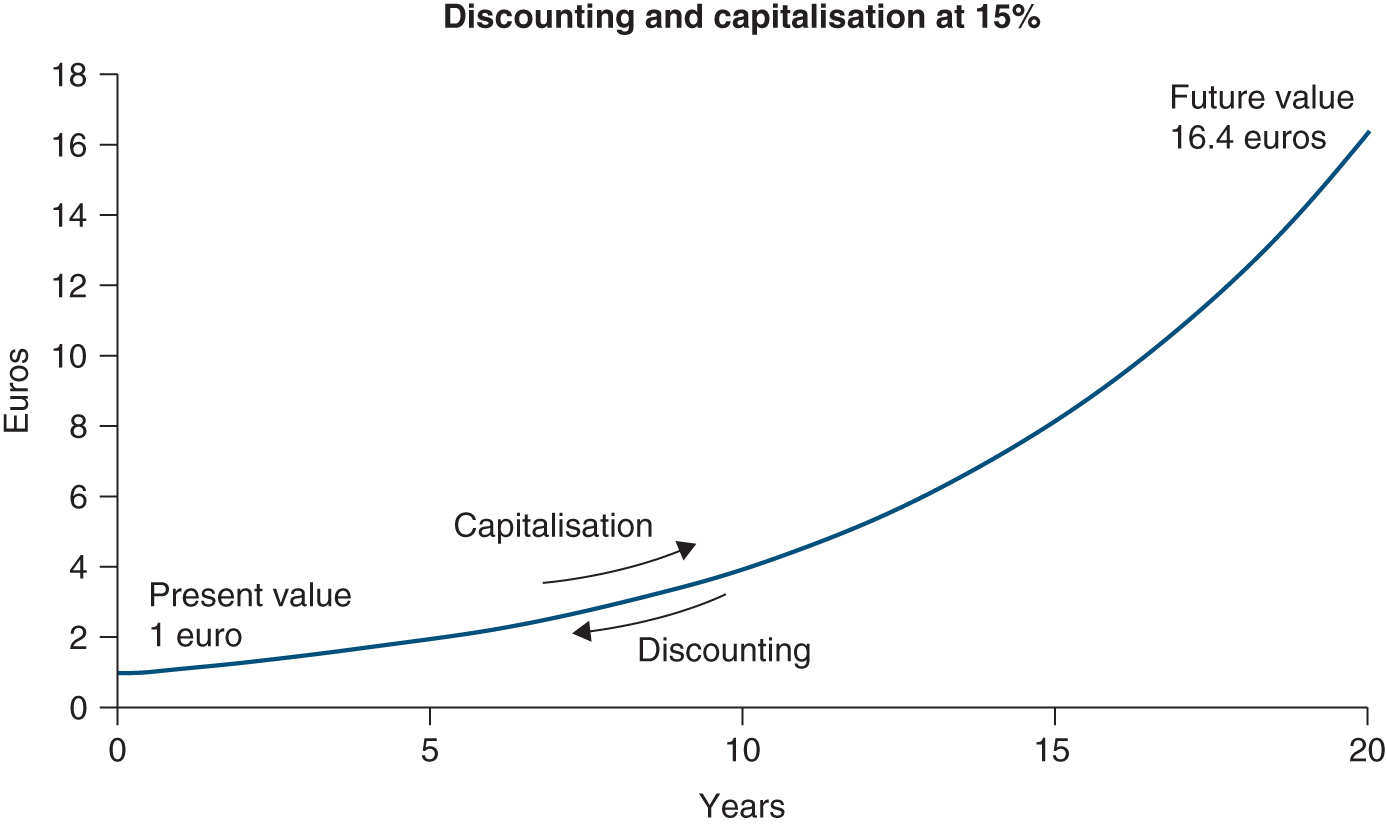

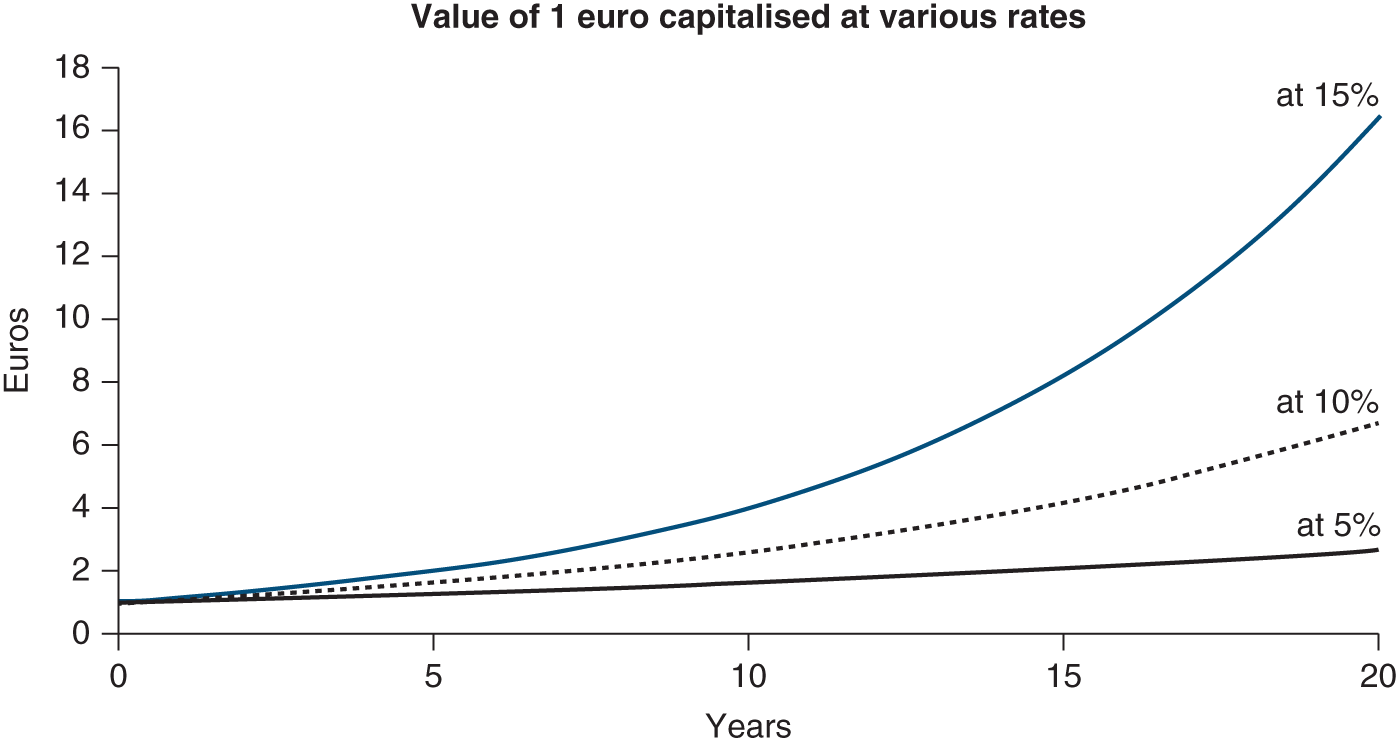

Over a long period of time, the impact of a change in the capitalisation rate on the terminal value looks as follows:

This increase in terminal value is especially important in equity valuations. The example we gave earlier of the businessman selling his company after 10 years is typical. The lower the income he has received on his investment, the more he would expect to receive when selling it. Only a high valuation would give him a return that makes economic sense.

The lack of intermediate income must be offset by a high terminal valuation. The same line of reasoning applies to an industrial investment that does not produce any income during the first few years. The longer it takes it to produce its first income, the greater that income must be in order to produce a satisfactory return.

Tripling one’s capital in 16 years, doubling it in 10 years or simply asking for a 7.177% annual return all amount to the same thing, since the rate of return is the same.

No distinction has been made in this chapter between income, reimbursement and actual cash flow. Regardless of whether income is paid out or reinvested, it has been shown that the slightest change in the timing of income modifies the rate of return.

To simplify, consider an investment of 100, which must be paid off at the end of year 1, with an interest accrued of 10. Suppose, however, that the borrower is negligent and the lender absent-minded, and the borrower repays the principal and the interest one year later than they should. The return on a well-managed investment that is equivalent to the so-called 10% on our absent-minded investor’s loan can be expressed as:

This return is less than half of the initially expected return!

It is not accounting and legal appearances that matter, but rather actual cash flows.

Section 16.2 DISCOUNTING

1/ WHAT DOES IT MEAN TO DISCOUNT A SUM?

Discounting into today’s euros helps us compare a sum that will not be produced until later. Technically speaking, what is discounting?

To discount is to “depreciate” the future. It is to be more rigorous with future cash flows than present cash flows, because future cash flows cannot be spent or invested immediately. First, take tomorrow’s cash flow and then apply to it a multiplier coefficient below 1, which is called a discounting factor. The discounting factor is used to express a future value as a present value, thus reflecting the depreciation brought on by time.

Consider an offer whereby someone will give you €1,000 in five years. As you will not receive this sum for another five years, you can apply a discounting factor to it, for example, 0.6. The present, or today’s, value of this future sum is then 600. Having discounted the future value to a present value, we can then compare it to other values. For example, it is preferable to receive 650 today rather than 1,000 in five years, as the present value of 1,000 five years out is 600, and that is below 650.

Remember that investors discount becausethey demand a certain rate of return. If a security pays you 110 in one year and you wish to see a return of 10% on your investment, the most you would pay today for the security (i.e. its present value) is 100. At this price (100) and for the amount you know you will receive in one year (110), you will get a return of 10% on your investment of 100. However, if a return of 11% is required on the investment, then the price you are willing to pay changes. In this case, you would be willing to pay no more than 99.1 for the security because the gain would have been 10.9 (or 11% of 99.1), which will still give you a final payment of 110.

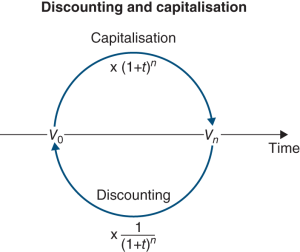

Discounting converts a future value into a present value. This is the opposite result of capitalisation.

Discounting converts future values into present values, while capitalisation converts present values into future ones. Hence, to return to the example above, €1,800,000 in 10 years discounted at 33.5% is today worth €100,000. €100,000 today will be worth €1,800,000 when capitalised at 33.5% over 10 years.

2/ DISCOUNTING AND CAPITALISATION FACTORS

To discount a sum, the same mathematical formulas are used as those for capitalising a sum. Discounting calculates the sum in the opposite direction to capitalising.

To get from €100,000 today to €1,800,000 in 10 years, we multiply 100,000 by (1 + 0.335)10, or 18. The number 18 is the capitalisation factor.

To get from €1,800,000 in 10 years to its present value today, we would have to multiply €1,800,000 by 1 / (1 + 0.335)10, or 0.056. 0.056 is the discounting factor, which is the inverse of the coefficient of capitalisation. The present value of €1,800,000 in 10 years at a 33.5% rate is €100,000.

More generally:

which is the exact opposite of the capitalisation formula.

1 / (1 + r)n is the discounting factor, which depreciates Vn and converts it into a present value V0. It is most often below 1, as discounting rates are generally positive.

Section 16.3 PRESENT VALUE AND NET PRESENT VALUE OF A FINANCIAL SECURITY

Owning a financial security such as a stock or a bond means owning the right to receive cash flows (dividend, interest, reimbursement, etc.) according to the specific terms of the security.

1/ FROM THE PRESENT VALUE OF A SECURITY …

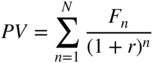

The present value (PV) of a security is the sum of its discounted cash flows, i.e.:

where Fn are the cash flows generated by the security, r is the applied discounting rate and n is the number of years for which the security is discounted.

All securities also have a market value, particularly on the secondary market. Market value is the price at which a security can be bought or sold.

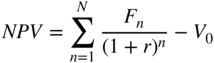

Net present value (NPV) is the difference between present value and market value (V0):

If the net present value of a security is greater than its market value, then it will be worth more in the future than the market has presently valued it at. Therefore, you will probably want to invest in it, i.e. to invest in the upside potential of its value.

If, however, the security’s present value is below its market value, then you should sell it at once (as its net present value is negative), for its market value is sure to diminish.

2/ … TO ITS FAIR VALUE

If an imbalance occurs between a security’s market value and its present value, then efficient markets will seek to re-establish balance and reduce net present value to zero. Investors acting on efficient markets seek out investments offering positive net present value, in order to realise that value. When they do so, they push net present value towards zero, ultimately arriving at the fair value of the security.

3/ APPLYING THE CONCEPT OF NET PRESENT VALUE TO OTHER INVESTMENTS

Up to this point, the discussion has been limited to financial securities. However, the concepts of present value and net present value can easily be applied to any investment, such as the construction of a new factory, the launch of a new product, the takeover of a competing company or any other asset that will generate positive and/or negative cash flows.

The concept of net present value can be interpreted in three different ways:

- The value created by an investment – for example, if the investment requires an outlay of €100 and the present value of its future cash flow is €110, then the investor has become €10 wealthier.

- The maximum additional amount that the investor is willing to pay to make the investment – if the investor pays up to €10 more, they have not necessarily made a bad deal, as they are paying up to €110 for an asset that is worth €110.

- The difference between the present value of the investment (€110) and its market value (€100).

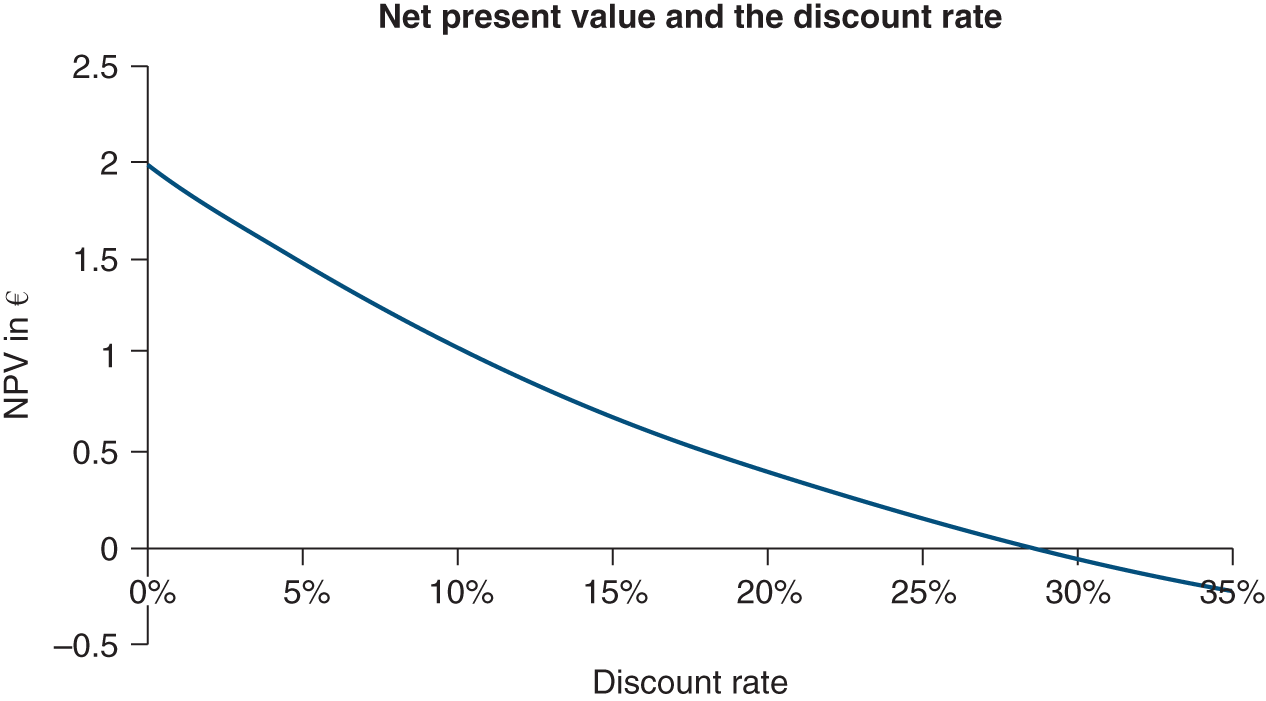

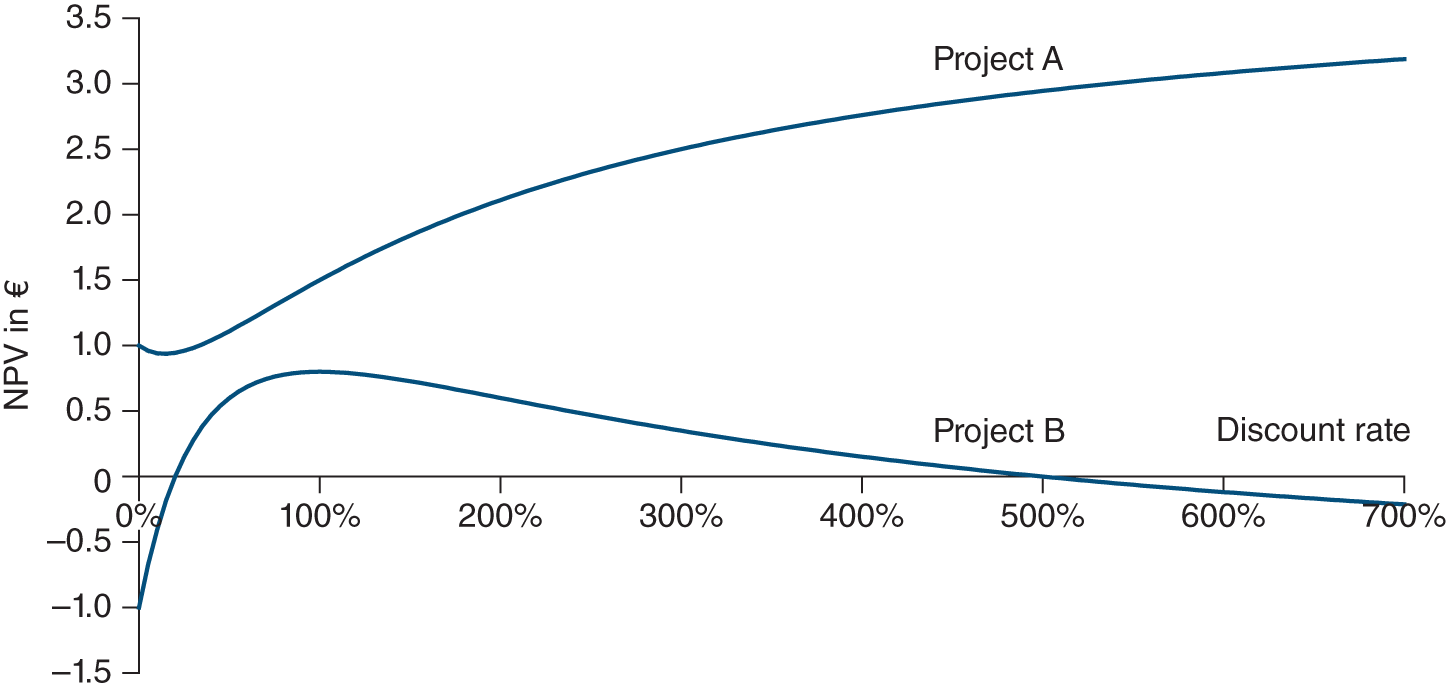

Section 16.4 WHAT DOES NET PRESENT VALUE DEPEND ON?

While net present value is obviously based on the amount and timing of cash flows, it is worth examining how it varies with the discounting rate.

The higher the discounting rate, the more future cash flow is depreciated and, therefore, the lower is the present value. Net present value declines in inverse proportion to the discounting rate, thus reflecting investor demand for a greater return (i.e. greater value attributed to time).

Take the following example of an asset (e.g. a financial security or a capital investment) with a market value of 2 and with cash flows as follows:

| Year | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Cash flow | 0.8 | 0.8 | 0.8 | 0.8 | 0.8 |

A 20% discounting rate would produce the following discounting factors:

| Year | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Discounting factor | 0.833 | 0.694 | 0.579 | 0.482 | 0.402 |

| Present value of cash flow | 0.67 | 0.56 | 0.46 | 0.39 | 0.32 |

As a result, the present value of this investment is 2.40.1 As its market value is 2, its net present value is 0.40.

If the discounting rate changes, the following values are obtained:

| Discounting rate | 0% | 10% | 20% | 25% | 30% | 35% |

|---|---|---|---|---|---|---|

| Present value of the investment | 4 | 3.03 | 2.39 | 2.15 | 1.95 | 1.78 |

| Market value | 2 | 2 | 2 | 2 | 2 | 2 |

| Net present value | 2 | 1.03 | 0.39 | 0.15 | −0.05 | −0.22 |

Which would then look like this graphically:

Section 16.5 SOME EXAMPLES OF SIMPLIFICATION OF PRESENT VALUE CALCULATIONS

For those occasions when you are without your favourite spreadsheet program, you may find the following formulas handy in calculating present value.

1/ THE VALUE OF AN ANNUITY F OVER N YEARS, BEGINNING IN YEAR 1

or:

For the two formulas above, the sum of the geometric series can be expressed more simply as:

So, if F = 0.8, r = 20% and n = 5, then the present value is indeed 2.4.

Further, ![]() is equal to the sum of the first n discounting factors.

is equal to the sum of the first n discounting factors.

2/ THE VALUE OF A PERPETUITY

A perpetuity is a constant stream of cash flows without end. By adding this feature to the previous case, the formula then looks like this:

As n approaches infinity in the formula of the previous paragraph, this can be shortened to the following:

The present value of a €100 perpetuity discounted back at 10% per year is thus:

A €100 perpetuity discounted at 10% is worth €1,000 in today’s euros. If the investor demands a 20% return, then the same perpetuity is worth €500.

3/ THE VALUE OF AN ANNUITY THAT GROWS AT RATE G FOR N YEARS

In this case, the F0 cash flow rises annually by g for n years.

Thus:

or:

Note: the first cash flow actually paid out is F0 × (1 + g).

Thus, a security that has just paid out 0.8, and with this 0.8 growing by 10% each year for the four following years, has – at a discounting rate of 20% – a present value of:

4/ THE VALUE OF A PERPETUITY THAT GROWS AT RATE G (GROWING PERPETUITY)

As n approaches infinity, the previous formula can be expressed as follows:

As long as r > g. The present value is thus equal to the next year’s cash flow divided by the difference between the discounting rate and the annual growth rate.

For example, a security with an annual return of 0.8, growing by 10% annually to infinity, has, at a rate of 20%, PV = 0.8 / (0.2 – 0.1) = 8.0.

SUMMARY

QUESTIONS

EXERCISES

ANSWERS

BIBLIOGRAPHY

NOTE

Chapter 17. THE INTERNAL RATE OF RETURN

A well-deserved return

If net present value (NPV) is inversely proportional to the discounting rate, then there must exist a discounting rate that makes NPV equal to zero.

To apply this concept to capital expenditure, simply replace “yield to maturity” by “IRR”, as the two terms mean the same thing. It is just that one is applied to financial securities (yield to maturity) and the other to capital expenditure (IRR).

Section 17.1 CALCULATING YIELD TO MATURITY

To calculate yield to maturity, make r the unknown and simply use the NPV formula again. The rate r is determined as follows:

To use the same example from Section 16.4:

In other words, an investment’s yield to maturity is the rate at which its market value is equal to the present value of the investment’s future cash flows.

In our illustration, the IRR is about 28.6% (see figure in Section 16.4).

Section 17.2 YIELD TO MATURITY AS AN INVESTMENT CRITERION

The yield to maturity is frequently used in financial markets because it represents for the investor the return to be expected for a given level of risk, which they can then compare to their required return rate, thereby simplifying the investment decision.

The decision-making rule is very simple: if an investment’s yield to maturity is higher than the investor’s required return, they will make the investment or buy the security. Otherwise, they will abandon the investment or sell the security.

In our example, since the yield to maturity (28.6%) is higher than the return demanded by the investor (20%), they should make the investment. If the market value of the same investment were 3 (and not 2), the yield to maturity would be 10.4%, and they should not invest.

Hence, at fair value, the yield to maturity is identical to the market’s required return. In other words, net present value is nil (this will be developed further in Chapter 26).

Section 17.3 THE LIMITS OF YIELD TO MATURITY OR IRR

With this new investment-decision-making criterion, it is now necessary to consider how IRR can be used vis-à-vis net present value. It is also important to investigate whether or not these two criteria could somehow produce contradictory conclusions.

If it is a simple matter of whether or not to buy into a given investment, or whether or not to invest in a project, then the two criteria produce exactly the same result, as shown in the example.

If the cash flow schedule is the same, then calculating the NPV by choosing the discounting rate and calculating the internal rate of return (and comparing it with the discounting rate) are two sides of the same mathematical coin.

The issue is, however, a bit more complex when it comes to choosing between several securities or projects, which is usually the case. Comparing several streams of cash flows (securities) should make it possible to choose between them.

1/ THE REINVESTMENT RATE AND THE MODIFIED IRR (MIRR)

Consider two investments A and B, with the following cash flows:

| Year | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|

| Investment A | 6 | 0.5 | |||||

| Investment B | 2 | 3 | 0 | 0 | 2.1 | 0 | 5.1 |

At a 5% discount rate, the present value of investment A is 6.17 and that of investment B is 9.90. If investment A‘s market value is 5, its net present value is 1.17. If investment B‘s market value is 7.5, its net present value is 2.40.

Now calculate the IRR. It is 27.8% for investment A and 12.7% for investment B. Or, to sum up:

| NPV at 5% | IRR% | |

|---|---|---|

| Investment A | 1.17 | 27.8 |

| Investment B | 2.40 | 12.7 |

Investment A delivers a rate of return that is much higher than the required return (27.8% vs. 5%) during a short period of time. Investment B‘s rate of return is much lower (12.7% vs. 27.8%), but is still higher than the 5% required return demanded and is delivered over a far longer period (seven years vs. two). Our NPV and internal rate of return models are telling us two different things. So, should we buy investment A or investment B?

At first glance, investment B would appear to be the more attractive of the two. Its NPV is higher and it creates the most value: 2.40 vs. 1.17.

However, some might say that investment A is more attractive, as cash flows are received earlier than with investment B and therefore can be reinvested sooner in high-return projects. While that is theoretically possible, it is the strong (and optimistic) form of the theory because competition among investors and the mechanisms of arbitrage tend to move net present values towards zero. Net present values moving towards zero means that exceptional rates of return converge towards the required rate of return, thereby eliminating the possibility of long-lasting high-return projects.

Given the convergence of the exceptional rates towards required rates of return, it is more reasonable to suppose that cash flows from investment A will be reinvested at the required rate of return of 5%. The exceptional rate of 27.8% is unlikely to be recurrent.

And this is exactly what happens if we adopt the NPV decision rule. The NPV in fact assumes that the reinvestment of interim cash flows is made at the required rate of return. The IRR assumes that the reinvestment rate of interim cash flows is simply the IRR itself. However, in equilibrium, it is unreasonable to think that the company can continue to invest at the same rate of the (sometimes) exceptional IRR of a specific project. Instead, it is much more reasonable to assume that, at best, the company can invest at the required rate of return.

However, a solution to the reinvestment rate problem of IRR is the modified IRR (MIRR).

So, by capitalising cash flow from investments A and B at the required rate of return (5%) up to period 7, we obtain from investment A in period 7: 6 × 1.0056 + 0.5 × 1.055, or 8.68. From investment B we obtain 2 × 1.056 + 3 × 1.055 + 2.1 × 1.052 + 5.1, or 13.9. The internal rate of return that allows for investment A in capitalising over seven years to reach 8.68 is 8.20%; it is often called modified IRR. For investment B, the modified IRR is 9.24%.

We have thus reconciled the NPV and internal rate of return models.

Some might say that it is not consistent to expect investment A to create more value than investment B, as only 5 has been invested in A vs. 7.5 for B. Even if we could buy an additional “half-share” of A, in order to equalise the purchase price, the NPV of our new investment in A would only be 1.17 × 1.5 = 1.76, which would still be less than investment B‘s NPV of 2.40. For the reasons discussed above, we are unlikely to find another investment with a return identical to that of investment A.

Instead, we should assume that the 2.5 in additional investment would produce the required rate of return (5%) for seven years. In this case, NPV would remain, by definition, at 1.17, whereas the internal rate of return of this investment would fall to 11%. NPV and the internal rate of return would once again lead us to conclude that investment B is the more attractive investment.

In fact, the NPV criterion is a better choice criterion than the IRR because it assumes that the intermediate flows of the investment are reinvested at the required rate of return (the discount rate), whereas in the calculation of the IRR they are assumed to be reinvested at that rate. The latter assumption is very strong because, if the IRR is higher than the required rate of return, it assumes that the company will always find projects that yield more than the required rate of return.

2/ MULTIPLE OR NO IRR

Finally, there are some rare cases where the use of the IRR leads to a deadlock. Consider the following investments:

| Year | 0 | 1 | 2 |

|---|---|---|---|

| Project A | 4 | −7 | 4 |

| Project B | −1 | 7.2 | −7.2 |

Project A has no IRR. Thus, we have no benchmark for deciding if it is a good investment or not. Although the NPV remains positive for all the discount rates, it remains only slightly positive and the company may decide not to do it.

Project B has two IRRs, and we do not know which is the right one. There is no good reason to use one over the other. Investments with “unconventional” cash flow sequences are rare, but they can happen. Consider a firm that is cutting timber in a forest. The timber is cut, sold and the firm gets an immediate profit. But, when harvesting is complete, the firm may be forced to replant the forest at considerable expense.

The IRR criterion does not allow for the ranking of different investment opportunities. It only allows us to determine whether one project yields at least the return required by investors. When the IRR does not allow us to judge whether an investment project should be undertaken or not (e.g. no IRR or several IRRs), the NPV should be analysed.

Section 17.4 EFFECTIVE ANNUAL RATE, NOMINAL RATES AND PROPORTIONAL RATES

We have just discovered the IRR, but many readers will be more aware of the interest rate, especially those planning to take out a loan. How can we reconcile the two?

Consider someone who wants to lend you €1,000 today at 10% for four years. This 10% means 10% per year and constitutes the nominal rate of return of your loan. This rate will be the basis for calculating interest, proportional to the time elapsed and the amount borrowed. Assume that you will pay interest annually, at the end of each annual period rather than at the beginning.

1/ THE CONCEPT OF EFFECTIVE ANNUAL RATE

Now what happens when interest is paid not once but several times per year?

Suppose that somebody lends you money at 10% but says (somewhere in the fine print at the bottom of the page) that interest will have to be paid on a half-yearly basis. For example, suppose you borrowed €100 on 1 January and then had to pay €5 in interest on 1 July and €5 on 1 January of the following year, as well as the €100 in principal at the same date.

This is not the same as borrowing €100 and repaying €110 one year later. The amount of interest may be the same (5 + 5 = 10), but the payment schedule is not. In the first case, you will have to pay €5 on 1 July (just before leaving on summer holiday), which you could have kept until the following 1 January in the second case. In the first case you pay €5, instead of investing it for six months as you could have done in the second case.

As a result, the loan in the first case costs more than a loan at 10% with interest due annually. Its effective rate is not 10%, since interest is not being paid on the benchmark annual terms.

To avoid comparing apples and oranges, a financial officer must take into account the effective date of disbursement. We know that one euro today is not the same as one euro tomorrow. Obviously, the financial officer wants to postpone expenditure and accelerate receipts, thereby having the money work for them. So, naturally, the repayment schedule matters when calculating the rate.

Which is the best approach to take? If the interest rate is 10%, with interest payable every six months, then the interest rate is 5% for six months. We then have to calculate an effective annual rate (and not for six months), which is our point of reference and our constant concern.

Two rates referring to two different maturities are said to be equivalent if the future value of the same amount at the same date is the same with the two rates.

In our example, the lender receives €5 on 1 July which, compounded over six months, becomes 5 + (10% × 5) / 2 = €5.25 on the following 1 January, the date on which they receive the second €5 interest payment. So, over one year, they will have received €10.25 in interest on a €100 investment.

Therefore, the effective annual rate is 10.25%. This is the real cost of the loan, since the return for the lender is equal to the cost for the borrower.

If the apparent rate (or nominal rate) (ra) is to be paid n times per year, then the effective annual rate (t) is obtained by compounding this nominal rate n times after first dividing it by n:

where n is the number of interest payments in the year and ra / n the proportional rate during one period, or t = (1 + ra / n)n − 1.

In our example:

The effective interest rate is thus 10.25%, while the nominal rate is 10%.

It should be common sense that an investment at 10% paying interest every six months produces a higher return at year end than an investment paying interest annually. In the first case, interest is compounded after six months and thus produces interest on interest for the next six months. Obviously, a loan on which interest is due every six months will cost more than one on which interest is charged annually.

The table below gives the returns produced by an investment (a loan) at 10% with varying instalment frequencies:

The effective annual rate can be calculated on any timescale. For example, a financial officer might wish to use continuous rates. This might mean, for example, a 10% rate producing €100, paid out evenly throughout the year on a principal of €1,000. As long as the financial officer is familiar with a rate corresponding to interest paid once a year, they will keep this rate as a reference rate.

By definition, IRR and yields to maturity are effective annual rates.

2/ THE CONCEPT OF PROPORTIONAL RATE

In our example of a loan at 10%, we would say that the 5% rate over six months is proportional to the 10% rate over one year. More generally, two rates are proportional if they are in the same proportion to each other as the periods to which they apply.

For example, 10% per year is proportional to 5% per half-year or 2.5% per quarter, but 5% half-yearly is not equivalent to 10% annually. Effective annual rate and proportional rates are therefore two completely different concepts that should not be confused.

Proportional rates serve only to simplify calculations, but they hide the true cost of a loan. Only the effective annual rate (10.25%/year) gives the true cost, unlike the proportional rate (10%/year).

When the time span between two interest payment dates is less than one year, the proportional rate is lower than the effective annual rate (10% is less than 10.25%). When maturity is more than a year, the proportional rate overestimates the effective annual rate. This is rare, whereas the first case is quite frequent on money markets, where money is lent or borrowed for short periods of time.

As we will see, the bond market practice can be misleading for the investor focusing on par value: bonds are sold above or below par value, the number of days used in calculating interest can vary, bonds may be repaid above par value, and so on. And, most importantly, on the secondary market, a bond’s present value depends on fluctuations in market interest rates.

Section 17.5 SOME MORE FINANCIAL MATHEMATICS: LOAN REPAYMENT TERMS

The first problem is how and when will you pay off the loan?

Repayment terms constitute the method of amortisation of the loan. Take the following examples.

1/ BULLET REPAYMENT

The entire loan is paid back at maturity.

The cash flow table would look like this:

| Period | Principal still due | Interest | Amortisation of principal | Annuity |

|---|---|---|---|---|

| 1 | 1,000 | 100 | 0 | 100 |

| 2 | 1,000 | 100 | 0 | 100 |

| 3 | 1,000 | 100 | 0 | 100 |

| 4 | 1,000 | 100 | 1,000 | 1,100 |

Total debt service is the annual sum of interest and principal to be paid back. This is also called debt servicing at each due date.

2/ CONSTANT (OR LINEAR) AMORTISATION

Each year, the borrower pays off a constant proportion of the principal, corresponding to 1/n, where n is the initial maturity of the loan.

The cash flow table would look like this:

| Period | Principal still due | Interest | Amortisation of principal | Annuity |

|---|---|---|---|---|

| 1 | 1,000 | 100 | 250 | 350 |

| 2 | 750 | 75 | 250 | 325 |

| 3 | 500 | 50 | 250 | 300 |

| 4 | 250 | 25 | 250 | 275 |

3/ EQUAL INSTALMENTS

The borrower may want to allocate a fixed sum to the service of debt (capital repayment and interests).

Based on the discounting method described previously, consider a constant annuity A, such that the sum of the four discounted annuities is equal to the present value of the principal, or €1,000:

This means that the NPV of the 10% loan is nil; in other words, the 10% nominal rate of interest is also the internal rate of return of the loan.

Using the formula from Section 16.5, paragraph 1, the previous formula can be expressed as follows:

A = €315.47. Hence, the following repayment schedule:

| Period | Principal still due | Interest | Amortisation of principal | Annuity |

|---|---|---|---|---|

| 1 | 1,000 | 100 | 215.47 | 315.47 |

| 2 | 784.53 | 78.45 | 237.02 | 315.47 |

| 3 | 547.51 | 54.75 | 260.72 | 315.47 |

| 4 | 286.79 | 28.68 | 286.79 | 315.47 |

In this case, the interest for each period is indeed equivalent to 10% of the remaining principal (i.e. the nominal rate of return) and the loan is fully paid off in the fourth year. Internal rate of return and nominal rate of interest are identical, as calculation is on an annual basis and the repayment of principal coincides with the payment of interest.

Regardless of which side of the loan you are on, both work the same way. We start with invested (or borrowed) capital, which produces income (or incurs interest costs) at the end of each period. Eventually, the loan is then either paid back (leading to a decline in future revenues or in interest to be paid) or held on to, thus producing a constant flow of income (or a constant cost of interest).

4/ INTEREST AND PRINCIPAL BOTH PAID WHEN THE LOAN MATURES

In this case, the borrower pays nothing until the loan matures. The sum that the borrower will have to pay at maturity is none other than the future value of the sum borrowed, capitalised at the interest rate of the loan:

This is how the repayment schedule would look:

| Period | Principal and interest still due | Amortisation of principal | Interest payments | Annuity |

|---|---|---|---|---|

| 1 | 1,000 | 0 | 0 | 0 |

| 2 | 1,100 | 0 | 0 | 0 |

| 3 | 1,219 | 0 | 0 | 0 |

| 4 | 1,331 | 1,331 | 1,331 | 1,464.1 |

This is a zero-coupon loan.

SUMMARY

QUESTIONS

EXERCISES

ANSWERS

BIBLIOGRAPHY

NOTE

****PART TWO. THE RISK OF SECURITIES AND THE REQUIRED RATE OF RETURN

Chapter 18. RISK AND RETURN

The spice of finance

Investors who buy financial securities face risks because they do not know with certainty the future selling price of their securities, nor the cash flows they will receive in the meantime. This chapter will try to explain and measure this risk, and also examine its repercussions.

Section 18.1 SOURCES OF RISK

There are various risks involved in financial securities, including:

- Industrial, commercial and labour risks, etc.

There are so many types of risk in this category that we cannot list them all here. They include lack of competitiveness, emergence of new competitors, technological breakthroughs, an inadequate sales network, strikes and so on. These risks tend to lower cash flow expectations and thus have an immediate impact on the value of the stock.

- Liquidity risk

This is the risk of not being able to sell an asset at its fair value as a result of either a liquidity discount or the complete absence of a market or buyers.

- Credit risk

This is the risk that a creditor will lose their entire investment if a debtor cannot repay them in full, even if the debtor’s assets are liquidated. Traders call this counterparty risk.

- Foreign exchange (FX) risk